The report argues that as governments and corporations increasingly compete for capital, gold is likely to underperform most risk assets and industrial commodities over the next three to five years

FinTech BizNews Service

Mumbai, July 18, 2026: Gold has enjoyed one of its strongest multi-year bull markets in history, supported by an extraordinary combination of low real interest rates, unprecedented monetary expansion, geopolitical uncertainty and persistent central bank buying. However, we believe the macroeconomic regime that underpinned this rally is gradually coming to an end. Over the next three to five years, gold is likely to underperform most risk assets and industrial commodities, with prices potentially remaining range-bound rather than extending the structural bull market witnessed over the past few years. Our bearish view is not based on the disappearance of geopolitical risks or the end of central bank purchases. Instead, it is rooted in a far more powerful structural force— the transition of the global economy from a "Savings Glut" regime to a "Capital Formation" regime. As argued in our earlier report Global Savings Reallocation to Broaden Capital Formation, the world is entering an era where governments and corporations will increasingly compete for capital to finance large-scale investment in defence, artificial intelligence, energy security, semiconductor manufacturing, industrial reshoring and infrastructure.

▪ From Savings Glut to Savings Grab:

For almost two decades following the Asian Financial Crisis and China's WTO accession, the global economy was characterized by an abundance of excess savings. Export-oriented economies such as China, Japan, Germany and major oil exporters consistently generated current account surpluses that were recycled into developed market financial assets, particularly US Treasuries. This persistent surplus capital depressed bond yields, compressed risk premia and allowed financial assets—including gold—to flourish in an environment of structurally cheap money. That world is changing rapidly. Instead of exporting excess savings, countries are increasingly deploying domestic capital to strengthen national resilience. Rising geopolitical fragmentation, deteriorating security architecture, supply-chain diversification, industrial policy and energy independence are encouraging governments to invest domestically rather than financing the deficits of other countries. Simultaneously, corporations are embarking on one of the largest capex cycles witnessed in decades as AI infrastructure, automation, cloud computing, semiconductor fabrication and electrification demand unprecedented levels of investment. The result is a structural transition from capital recycling towards capital formation.

▪ Capital is Becoming Scarcer:

Gold has historically performed best when capital is abundant. The previous decade was characterized by excess liquidity searching for financial assets. The coming decade is likely to be characterized by competition for savings. The world's pool of savings is no longer expanding rapidly while investment requirements are rising sharply. The charts in our previous report illustrate this transition clearly. Global gross capital formation is projected to steadily rise while national savings either stagnate or decline across major developed economies. This widening gap implies that future investment will increasingly require higher returns to attract capital. Unlike the post-2008 period when central banks actively suppressed real yields through quantitative easing, governments are now issuing increasing amounts of debt to finance defence spending, infrastructure, industrial policy and strategic investments. Simultaneously, corporations require enormous financing to fund AI data centres, semiconductor fabs, power grids and manufacturing capacity. The equilibrium price of capital therefore rises. Higher demand for capital inevitably translates into higher real interest rates.

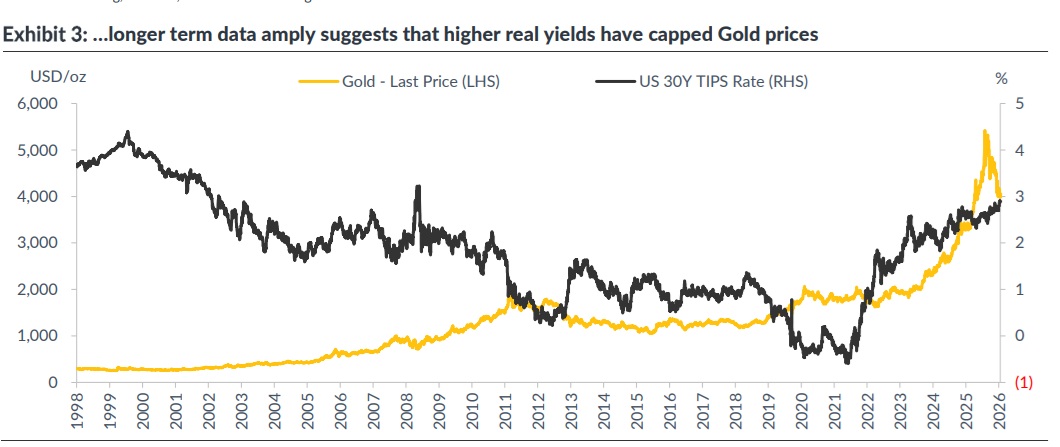

Higher Real Yields to be Gold's Biggest Headwind:

Gold’s attractiveness rises when investors earn very little from holding cash or government bonds. Conversely, when real yields rise, the opportunity cost of holding a non-yielding asset increases substantially. Historically, the relationship between US real yields and gold has been one of the most reliable macro relationships across asset classes. Every major period of sustained gold underperformance coincided with rising or elevated real interest rates. Our Capital Formation thesis suggests that real yields may remain structurally higher than markets currently expect. Rather than representing a temporary cyclical phenomenon, elevated real rates could become a defining feature of the next investment regime as governments and corporations increasingly compete for scarce global savings. Real sovereign yields across major economies have already begun normalizing after years of financial repression, reflecting the growing global demand for capital. If this structural repricing continues, it will become increasingly difficult for gold to generate sustained upside.

▪ The New Winners Are Productive Assets, Not Defensive Stores of Value:

Every investment regime rewards different asset classes. The Savings Glut era rewarded duration assets, longdated bonds, growth stocks and gold because abundant liquidity and falling discount rates continually expanded valuations. The emerging Capital Formation era is fundamentally different. Capital increasingly flows toward productive investments capable of generating future cash flows rather than passive stores of value. Industrial companies, capital goods manufacturers, electrical equipment suppliers, defence companies, engineering firms, utilities, semiconductor equipment manufacturers and copper producers become direct beneficiaries of rising investment spending. Even infrastructure assets gain because they participate directly in the global capex cycle. Gold, by contrast, does not benefit from rising investment activity. It neither participates in productivity improvements nor generates incremental earnings from expanding capital expenditure. As investors increasingly allocate capital toward productive assets capable of compounding earnings through higher investment spending, the relative attractiveness of Gold diminishes.

▪ Industrial Commodities Could Outperform Precious Metals:

Forces supporting higher capital formation are likely to create sustained demand for industrial commodities. Copper, aluminium, electrical equipment, specialty steel, uranium, power infrastructure and engineering services all stand to benefit directly from AI infrastructure, electrification, defence manufacturing and reshoring initiatives. Gold occupies the opposite side of this equation. Unlike industrial metals whose consumption rises with investment spending, gold demand remains primarily safe-haven appetite driven. Therefore, the very macro forces lifting industrial commodity demand simultaneously increase real yields—the principal headwind for Gold. The commodity leadership of the coming decade may therefore shift toward industrial metals.

▪ Central Bank Buying May Cushion—but Not Drive—the Next Leg:

One of the strongest bullish arguments for gold has been persistent central bank accumulation. While central banks may continue diversifying reserves amid geopolitical fragmentation, reserve diversification alone is unlikely to offset the powerful macro effects of structurally higher real interest rates. Central bank purchases can provide a valuation floor during periods of market stress, but they would not create sustained secular bull markets unless supported by favourable monetary conditions. In other words, central bank buying may prevent a collapse in Gold prices but is unlikely to generate another decade of outsized returns if real yields continue moving higher.

▪ Gold Prices to be Stuck in a Rut:

Rather than expecting a dramatic collapse in Gold prices, investors should prepare for a prolonged period of relative underperformance. Gold could increasingly resemble a lengthy phase of sideways movement punctuated by short-lived rallies during geopolitical shocks. Such episodes may continue to occur, but they are unlikely to establish new secular highs if the underlying structural environment remains characterized by elevated real yields and expanding capital investment. Meanwhile, sectors directly linked to global capital formation could continue attracting incremental capital.