The inverse correlation between US 10 year real rate & Gold prices (USD) seems to have broken due to increasing uncertainty and world moving away from US treasuries & towards Gold. Investment in Gold should be done from the asset allocation point of view.

FinTech BizNews Service

Mumbai, February 21, 2025: Motilal Oswal Private Wealth has come out with Alpha Strategist Report 2025, authored by Ashish Shanker, MD & CEO, Motilal Oswal Wealth. The report observes with its market outlook: “We expect the markets to remain in the such corrective to consolidation phase for the next 3 to 4 months and such phases of the market should be considered for gradual accumulation. For equity, investors can increase allocation by implementing a lump sum investment strategy for Hybrid & Large Cap Equity Oriented fund and staggered approach over the next 6 months for Flexi, Mid and Small Cap Strategies.”

The report contains main points as follows:

The global financial as well as geopolitical landscape is witnessing significant changes, driven by evolving macroeconomic trends and policy decisions.

One of the key shifts is the rise in the U.S. interest rates, influenced by factors such as rising fiscal deficit, persistent inflation, and uncertainty surrounding Trump’s policies. This is of significance because yields are persisting at levels last seen during 2007-08 period and markets expect yields to remain higher for longer as indicated by Fed Futures probabilities. Japan, another major economy and an important carry trade participant, seems to be also on the path for higher rates after a period of ultra-loose monetary policy for more than 15 years.

Second major change is the move towards deglobalization as evident from the recent imposition of tariffs by U.S., aimed at protecting domestic interests. While the current announcements are milder than anticipated and seem more like a negotiation strategy, such actions will lead to disruptions in global trade and further fuel the momentum towards deglobalization.

Rising fears of global trade war amidst increasing likelihood of higher-for-longer interest rates have strengthened the Dollar Index to above 108 levels, triggering risk-off mode and FII outflows from emerging markets. INR has also depreciated ~4% since Sep'24 and almost touched the 88 mark before RBI intervention got rupee back below 87.

Indian Union budget highlighted continuous focus on fiscal prudence by targeting 4.4% fiscal deficit for FY26 (vs 4.8% in FY25RE). However this time, by providing the income tax cuts, government has given preference to consumption boost over capital expenditure – a shift from the earlier budgets. This move is one of the biggest in terms of tax forgone due to income tax cut by the exchequer and is likely to result in additional ~1 Lac Crs in the hands of the taxpayer. We expect this to provide the much needed boost to consumption demand from middle class salaried population.

These Changing Norms – Higher-for-longer interest rates, Deglobalization gaining momentum and Govt of India’s shift from Capex to Consumption underscore the emerging trends which are significantly different from what investors witnessed in the last decade and hence highlight the need for adaptive strategies in navigating financial markets today.

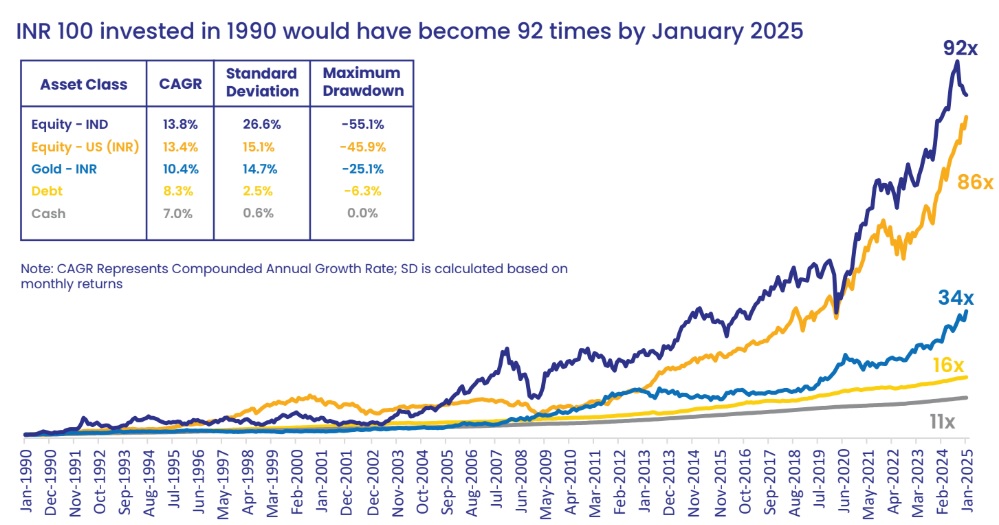

Amidst these uncertainties, Indian equity markets have seen sharp corrections due to continuous FII outflow, rising US Yield and weak earnings growth. Individual stock level correction is much more severe than indices suggest as average price fall in stocks from the all-time high is almost twice the index fall. ~75% stocks from Mid Cap 150 & Small Cap 250 Index are down by more than 20% from all-time high. However, despite corrections, Mid Cap and Small Cap valuations continue to remain expensive, while Large Caps look more reasonable trading below the 10 year average forward PE multiple.

We expect the markets to remain in the such corrective to consolidation phase for the next 3 to 4 months and such phases of the market should be considered for gradual accumulation. For equity, investors can increase allocation by implementing a lump sum investment strategy for Hybrid & Large Cap Equity Oriented fund and staggered approach over the next 6 months for Flexi, Mid and Small Cap Strategies.

On fixed income, Govt's commitment to fiscal consolidation path resulting in flat net borrowing and RBI's OMO purchase are likely to keep yields under check from demand supply perspective. However Yield Gap between US 10 Yr and India 10 Yr is at ~220 bps vs long term average of ~400-450 bps and there is very little room for the spread to compress further.

After a softening of ~60 bps during last 1-1.5 years, we believe that the duration play is in its last leg and long term yields to remain higher for longer and hence duration can be exited fully. Actions by RBI on rate cuts and liquidity, are likely to result into steepening in yield curve. We recommend fixed income portfolio to be Overweight on Accrual Strategies.

The inverse correlation between US 10 year real rate & Gold prices (USD) seems to have broken due to increasing uncertainty and world moving away from US treasuries & towards Gold. Investment in Gold should be done from the asset allocation point of view.