India’s tech ecosystem moved ahead of Germany and France to rank as the 4th most funded globally, raising $11.7B in FY26.

FinTech BizNews Service

Mumbai, April 9, 2026: Tracxn, a leading market intelligence platform, has released its India Tech Annual Funding Report 2026. The proprietary report provides comprehensive insights into the Indian tech ecosystem, highlighting funding activity, sector performance, IPOs, acquisitions, investor participation, major players, and the key trends shaping the sector’s landscape in 2025.

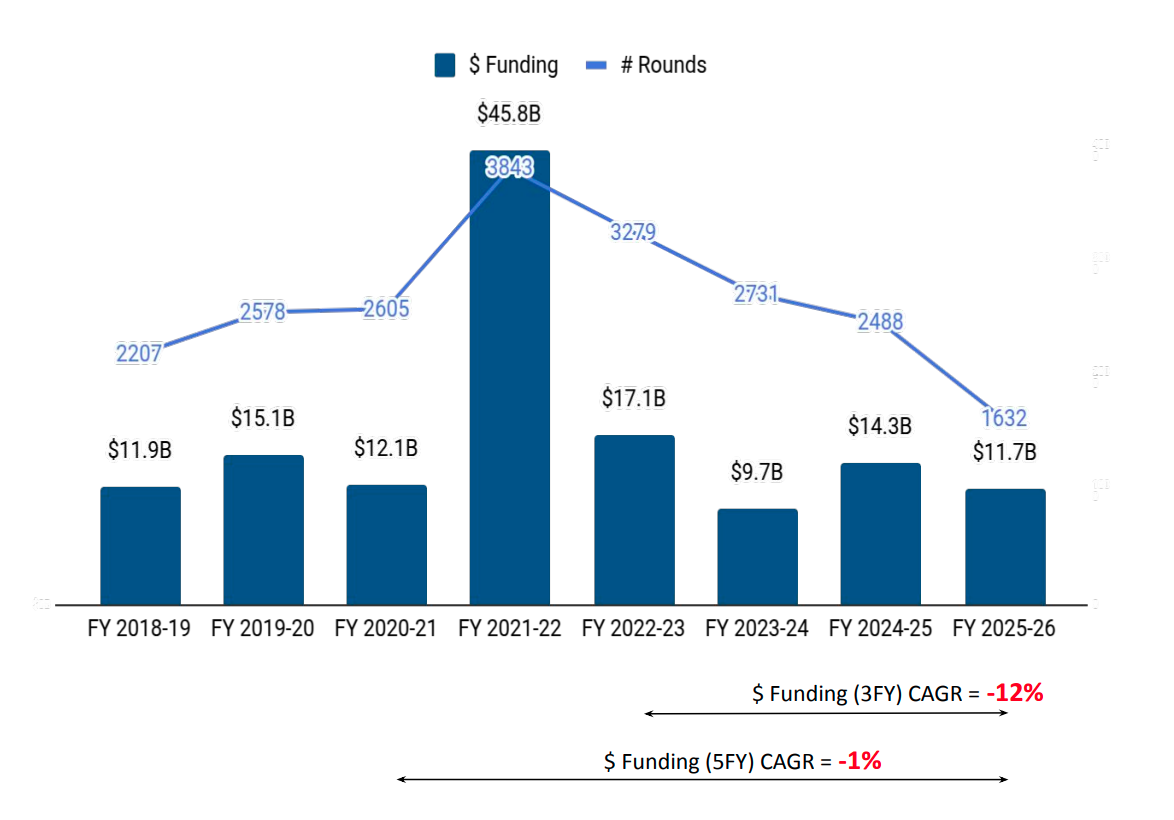

Image: Q-o-Q Funding Trends (Note: Funding includes only Equity Funding. It excludes Debt, Grant, Post-IPO and ICO funding.)

According to the report, India’s startups raised $11.7B in FY 2025-26, marking an 18% decline from $14.3B in FY 2024-25 but a 20% increase compared to $9.7B raised in FY 2023-24. India ranked as the fourth-highest funded country globally in FY 2025-26, behind the United States, the United Kingdom, and China, and ahead of Germany and France.

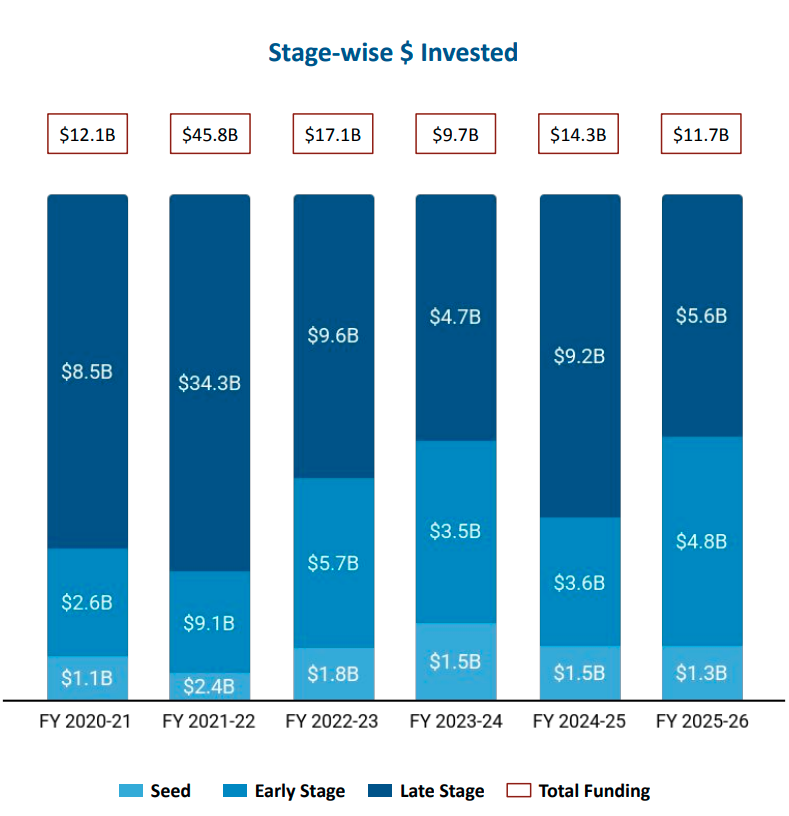

Image: Q-o-Q Stage-wise Funding Trends (Note: Seed includes Seed, Angel rounds. Early Stage includes Series A,B rounds. Late Stage includes Series C+, PE, Pre-IPO rounds)

Funding trends varied across stages. Seed-stage startups raised $1.3B in FY 2025-26, marking a 15% decline from $1.5B raised in FY 2024-25 and in FY 2023-24. Early-stage funding showed strong momentum, rising to $4.8B in FY 2025-26, a 33% increase from $3.6B raised in FY 2024-25, and a rise of 37% compared to $3.5B raised in FY 2023-24.. Late-stage startups raised $5.6B in FY 2025-26, marking a 38% decline from $9.2B raised in FY 2024-25, but a 18% increase compared to $4.7B raised in FY 2023-24.

Commenting on the insights, Neha Singh, Co-Founder of Tracxn, said, “While overall funding saw moderation,, the strong momentum in early-stage investments highlights continued investor confidence in startups building differentiated and scalable solutions. The sustained traction in sectors such as Enterprise Applications, FinTech, and Retail reflects the growing importance of technology-led transformation across industries. Additionally, increased IPO activity and unicorn creation indicate improving maturity within the ecosystem, with companies demonstrating stronger fundamentals, capital efficiency, and clearer paths to profitability.”

In FY 2025-26, India witnessed 13 funding rounds of $100M+, compared to 23 such rounds in FY 2024-25 and 13 in FY 2023-24. Large deals were driven primarily by the Enterprise Infrastructure, Enterprise Applications, and Fintech with companies raising notable capital including Nxtra’s $710M PE round, Neysa’s $600M Series B round, and Inox Clean Energy’s $344M Series D funding.

The report highlights that Enterprise Applications, FinTech, and Retail emerged as the top-performing sectors in FY 2025-26. Enterprise Applications received $3.6B in FY 2025-26, same as in FY 2024-25, but a 23% increase from $2.9B raised in FY 2023-24. FinTech secured $2.4B in funding, marking a 14% increase from $2.1B in FY 2024-25 and a 27% rise compared to $1.9B raised in FY 2023-24. Retail raised $2.4B in FY 2025-26, registering a 32% decline from $3.5B in FY 2024-25 and a 19% decrease compared to $2.9B raised in FY 2023-24.

India’s tech startup ecosystem recorded 129 acquisitions in FY 2025-26, compared to 151 acquisitions in FY 2024-25, marking a 15% decline in acquisitions activity during the year. The number of acquisitions also saw a 2% drop compared to 132 acquisitions in FY 2023-24. Resulticks stood out with a $2B acquisition by Diginex, making it the highest-valued acquisition in FY 2025-26, followed by Brahma’s acquisition by Polymarket at a deal value of $1.2B.

On the IPO front, India Tech recorded 47 IPOs in FY 2025-26, marking a 52% increase over 31 IPOs in FY 2024-25 and a 47% rise compared to 32 IPOs in FY 2023-24. Major IPOs during the year included Lenskart, Groww, and Meesho.

There were 6 unicorns created in FY 2025-26, reflecting a 50% increase compared to 4 in FY 2024-25, and in FY 2023-24.

City-wise, Bengaluru accounted for 33% of total funding, maintaining its position as India’s leading startup hub, followed by Mumbai with 21% of total funding.

On the investor front, Inflection Point Ventures, Rainmatter, and Venture Catalysts emerged as the most active seed-stage investors in the India Tech ecosystem in FY 2025-26. Peak XV Partners, Accel, and Lightspeed Venture Partners led early-stage investments, while Sofina, Elev8, and Lathe Investment were the top late stage investors in India Tech ecosystem for FY 2025-26.