Muted quarter; navigating mixed signals in FY2027, as per a Kotak Institutional Equities Report

FinTech BizNews Service

Mumbai, April 2, 2026: The latest special Kotak Institutional Equities report focuses on IT Services and estimates muted 4QFY26 revenue growth across many companies in the sector .

Muted quarter; navigating mixed signals in FY2027

4QFY26 performance is likely to remain muted, but with a stable to improving yoy growth trajectory. A sharp depreciation of INR against USD means many companies will report double-digit yoy earnings growth. FY2027 guidance will be shaped by geopolitical uncertainty from the Iran war and increasing revenue deflation from GenAI-led programs. We expect Infosys to guide to 3-5% revenue growth for FY2027 with stable margins, while HCLT is likely to guide to 3-5% overall growth with a modest 50 bps expansion in its EBIT margin band. Tech Mahindra, TCS, Infosys and Coforge are our key picks.

Muted 4QFY26 with stable to accelerating yoy growth trajectory

We expect muted 4QFY26 revenue growth across many companies in the sector, although the yoy growth profile should improve for several companies. The quarter benefits from the absence of furloughs, particularly in BFSI and retail, although this is partly offset by a lower number of working days. The financial services vertical is likely to lead growth sequentially. We expect TCS to lead revenue growth among Tier-1 companies, while Persistent will lead the charge among mid-tier companies.

EBIT margin—steady expansion helped by currency

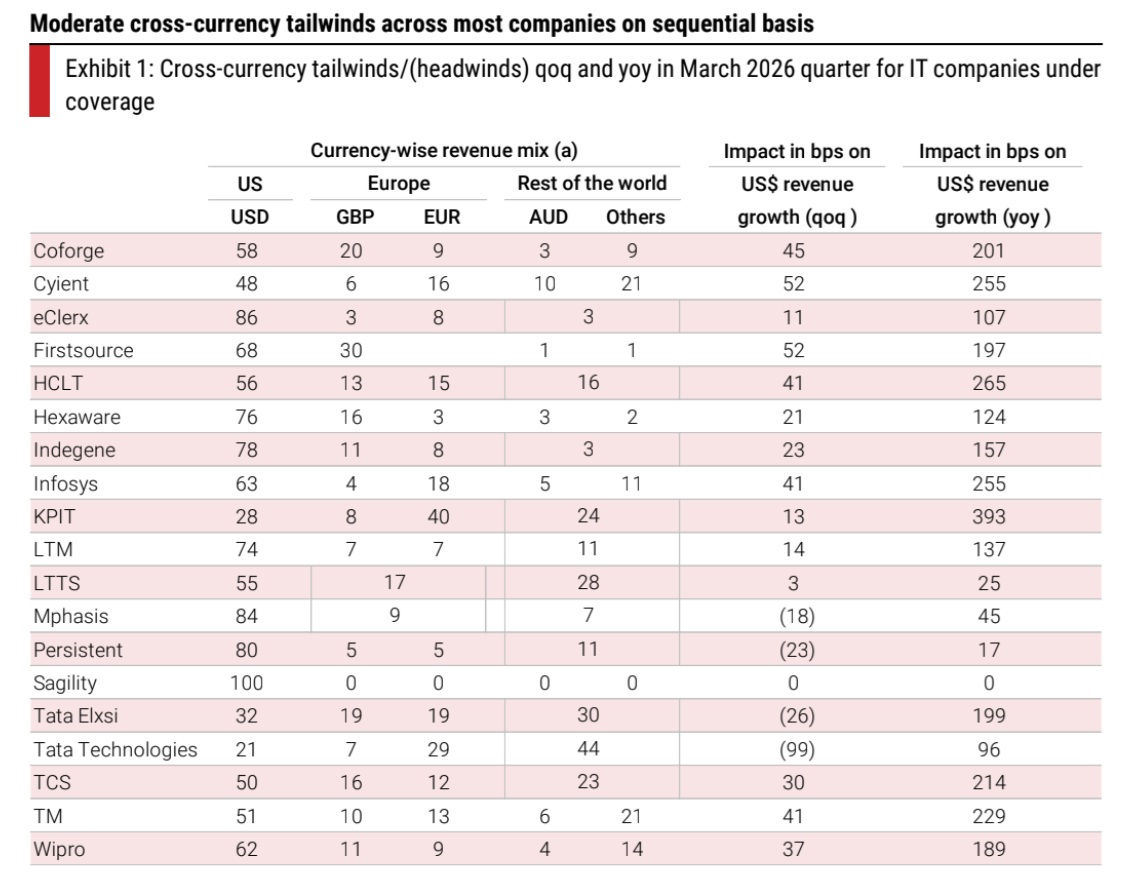

We expect 40-320 bps yoy increase in EBIT margin among top-6 IT helped by 6.5% depreciation against USD. Wipro and HCLT would report ~20-30 bps yoy declines. On a sequential basis, rupee has depreciated by 3.5%. We expect stable margins to increasing margins. Translation of rupee depreciation will vary depending on magnitude of hedging. Large companies have marginal hedging and will result in immediate translation of currency into earnings. A few companies such as LTM, LTTS, Coforge, Persistent and Hexaware have hedges varying from 12 months to three years and will report hedge losses.

FY2027 guidance—influenced by many factors, 3-5% for Infosys and HCLT

Two factors dominate the outlook. First, elevated geopolitical risk from the Iran war adds uncertainty to global macro conditions and enterprise spending visibility. Second, GenAI-driven productivity programs are increasingly deflationary in nature. These factors are likely to cap headline growth guidance despite reasonable deal pipeline. Our base-case expectations assume some de-escalation in geopolitical conditions; a prolonged or intensifying conflict would pose downside risks to both demand assumptions.

Within this context, we expect Infosys to guide to 3-5% revenue growth for FY2027. We bake in 75 bps from Versent acquisition into the guidance noting that management expected the deal to close by the end of the fiscal year. HCLT is likely to guide to 3-5% overall revenue growth, supported by its services mix and large deal ramp-ups. We expect service revenue growth in 4-6% band. HCLT might raise its EBIT margin guidance band by around 50 bps to 17.5-18.5% from 17-18% in FY2026E.

We expect Wipro to guide for (-)2 to 0% revenue growth for June 2026 quarter indicating share losses, delayed ramp up of large deals and pricing pressure.

Stock view—cheap but with many uncertain parts

Stocks have corrected 19-39% in the past two months. At the same time, macro headwinds pose another challenge for the sector in addition to GenAI risks. The current stock prices of TCS and TechM reflect low growth expectations. The stocks trade at ~16X FY2028E earnings and are available at ~5% payout yield and ~5-6% FCF yield. TechM has the potential to consistently grow above industry growth. Coforge trades at inexpensive valuation of 18X FY2028E EPS.

Hedging by companies to result in variance on quarterly numbers

Mid-tier IT companies have largely locked in their FY2027 P&L through hedging, with hedge rates typically in the Rs89-91/US$ range. As a result, currency benefits are unlikely to fully flow through to net profit for several mid-cap companies, even as reported EBIT margins improve, creating a divergence between operating performance and bottom-line growth in FY2027. LTM has the highest hedge book, with outstanding hedges of US$4.37 bn at an average rate of Rs91.29 as of the December 2025 quarter. Coforge, Persistent, Mphasis and Hexaware have hedge coverage extending up to 12 months, with hedge quantum typically ranging 50-90% of expected net cash inflows. From an accounting perspective, Coforge and Mphasis recognize cash flow hedge-related gains or losses within the revenue line, while Hexaware and Persistent report these impacts under other income

Factors influencing FY2027 revenue growth guidance

Our FY2027 guidance assumptions for Infosys and HCL Technologies embed a base case where current US-Iran hostilities are scaled down by the time companies issue formal guidance, avoiding a sharp deterioration in global enterprise spending sentiment. We assume geopolitical risk remains an overhang but does not translate into broad-based discretionary freezes. On GenAI, our framework assumes a measured transition from pilots to production, with productivity-led deflation within existing contracts outweighing net-new revenue creation in the near term. Commercial models are expected to evolve gradually toward outcome-linked constructs, without abrupt resets to pricing or margin structures in FY2027. Any escalation in geopolitical conflict would pose downside risk to both growth embedded in current guidance expectations.

Key things to watch for:

4 | Agentic AI and impact on decision making. A key question is whether progress on agentic AI has materially altered client decision making timelines. Our checks did that in some cases, CIOs and procurement teams appear to be slowing decision-making as they reassess how quickly agentic AI could alter services delivery. At this stage, the impact is limited to greater caution and review rather than a broad-based shift in spending behavior. |

4 | Hiring, workforce mix and skill obsolescence. Hiring commentary will be closely watched, not just on volumes but on workforce rebalancing. Skill sets in a few areas are becoming less relevant in an agentic AI-led delivery model, necessitating replacement with next generation competencies in data engineering, AI orchestration, model operations and domain-led solutioning. The pace and cost of this transition will have margin and execution implications. |

4 | GenAI programs moving from POC to production. Disclosures on the share of GenAI engagements that have moved into production will be important. Equally critical is whether these programs are net new revenue streams or largely represent deflation of existing application, infrastructure or BPO work. This distinction will shape medium-term growth expectations. |

4 | Rising M&A intensity despite deflation risks. M&A activity has picked up across companies, which appears counterintuitive given that some acquired competencies themselves face GenAI-led deflation risk. Management articulation on the strategic rationale, integration timelines and durability of acquired capabilities will be scrutinized closely. |

Limited demand improvement in auto ERD

Auto OEMs remain under significant transformation pressures to meet regulatory timelines as well as evolving consumer demand. While US tariffs impacted business in FY2026, there is limited respite in FY2027 due to limited demand improvement, reprioritization of spends and geo-political uncertainties, which if prolonged could be an incremental headwind. Recovery hopes of most ESPs are pinned on increased offshoring by large European OEMs, which have been significantly delayed on planned transformation programs. US PV business outlook remains muted due to reprioritization of large programs and OEMs, with those with higher exposure to the market having announced material write-down of investments. CV OEMs demand is likely to be led by autonomy and alternate powertrains to meet EPA27 norms and is likely to support growth in the near term. Aerospace remains resilient, with demand led by MRO spends with limited visibility of new platform development program timelines. Industry 4.0 and sustainability initiatives would drive spends among energy & utilities vertical clients.

Early signs of disruption emerging in parts of BPO

BPO pure-play companies with significant customer management services are likely to face headwinds in their existing businesses as AI agents’ adoption picks up among enterprises. We note that agentic capabilities have improved as compared to 6-12 months ago, which would prompt enterprise interest in more wide-spread deployments for administrative activities. Deal conversion timelines remain longer than expected for large deals, indicating greater scrutiny of spends and exploring avenues to improve efficiencies. Healthcare BPO spends are likely to remain under pressure, primarily among health plans participating in federal programs. We bake in some margin pressure for companies due to increased asks for greater productivity by clients. Companies participating in large outcome-based deals would need to adequately bake-in efficiencies. While more wide-spread AI-infusion can help in generating higher efficiencies, aggressive assumption of productivity improvement would hurt medium-term profitability. Sharp rupee depreciation, if sustained, can be a near-term offset.

Discussion on individual companies

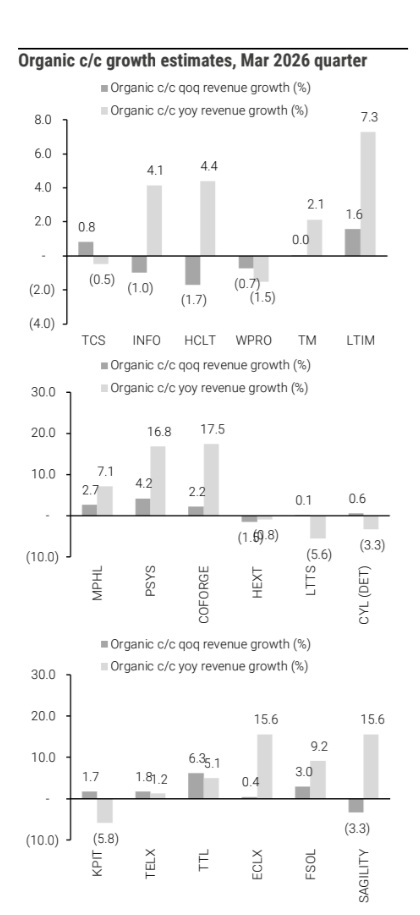

4 | TCS. We forecast 1.2% growth in c/c contributed by 0.8% on organic basis and 40 bps contribution from Coastal cloud acquisition. We expect international business to grow faster and believe that India business will decline marginally. We expect stable EBIT margin. Headwind of wage revision and Coastal cloud acquisition will likely be offset by rupee depreciation. We expect deal TCV of US$9-10 bn, down on yoy comparison. Note that the base quarter had benefit of a large deal renewal. Deal TCV will likely decline 22% yoy and stable on qoq basis. Note there was no mega-deal closure in the quarter. Focus will be on company's renewed aggression and investments to accelerate growth. We expect investor focus on: (1) progress in agentic AI in the past three months and whether than leads to change in AI deflation assumption, (2) timeframe for convergence of growth with peers and that the factors that may drive the same, (3) impact of GCC ramp-up on growth of companies and GCC as a growth lever, (5) progress on planned data center investments, (6) areas of strategic importance for inorganic investments, especially after a couple of acquisitions in the past two quarters and (7) margin aspirations in light of elevated competitive intensity. |

4 | Infosys. We forecast revenue decline of 1% qoq primarily due to lower billing days and seasonal weakness. We expect stable revenues from sale of third-party items. We expect stable margins as benefits of rupee depreciation is offset by higher visa costs. Sharp decline in other income after completion of buyback to result in moderate net profit growth. We expect large deal TCV of US$2.5-2.75 bn, stable on yoy comparison. We believe Infosys will guide for 3-5% growth in revenues including Versent acquisition and 2.25-4.25% on organic basis. Hurdle rate to achieve the revenue growth guidance stands at CQGR of 1.2-1.9% (0.8-1.6% CQGR on organic basis). We expect investor focus on: (1) impact of Iran war and GenAI deflation on growth prospects, (2) change in decision-making pace of clients due to rapid improvement in agentic capabilities, (3) willingness to take up large transformation programs that are margin dilutive initially, (4) percentage of programs that have moved from PoC to production, and (5) incremental benefits that can accrue from Project Maximus. |

4 | HCL Tech. We forecast c/c revenue decline of 1.7% and yoy growth of 4.4%. Growth will be led by IT business (+1.1%), offset by seasonal decline in products revenues. Expect reported EBIT margin of 17.7% and underlying EBIT margin of 18.5%. EBIT will margin has impact of 80 bps from restructuring charge. Tailwinds of rupee depreciation will likely be offset by headwinds from wage revision (50 bps). We expect healthy TCV of deal wins in US$2.5 bn range. Focus will be on FY2027E revenue guidance. Helping HCLT will be a mega-deal ramp-up and higher exposure to lower AI-hit IMS revenues. We expect the company to guide for 3-5% revenue growth excluding acquisition of HPE's telco solutions group. Services business revenue growth guidance is likely to be in 4-6% range, implying 0.6-1.4% CQGR. We expect HCLT to raise margin guidance band to 17.5-18.5% for FY2027E, up from 17-18% earlier. FY2026 margin guidance band was impacted by 60 bps due to restructuring charge. In addition, recent rupee depreciation will also aid margins. We expect investor focus on: (1) pace of new revenues pools possible with GenAI that can offset revenue deflation, (2) how the company has baked in recent deterioration in macro in the guidance, (3) profitability in cost take-out and vendor consolidation deals, (4) GenAI risks to products business, and (5) kind of demand environment required for growth to accelerate to high single digit. |

4 | Wipro. We expect overall revenue growth of 0.9% c/c qoq, which includes 160 bps contribution from the DTS acquisition. On organic basis, we expect revenue decline of 0.7%. We expect broadly stable EBIT margins. Headwind from wage revision for a month and DTS acquisition will likely to be offset by rupee depreciation. We expect revenue guidance of (-)2 to 0% growth. Loss of a large deal and pricing pressure will lead to weak quarter. Wipro has distributed excess cash in the past through buyback. Even as the company has increased dividend payout ratio, we do not think the approach to distributing excess cash will change. Expect focus on buyback announcement. We expect investor focus on (1) reasons for loss of a large client, (2) pricing pressure in the healthcare vertical, (3) timelines for catch up of growth with peers, (4) Wipro's point of view on agentic AI and readiness to be deployed in client environment, and (5) GCC growth strategy. |

4 | TechM. We forecast flat revenues for the quarter. December 2025 quarter had benefit of pull forward of revenues in the manufacturing vertical, which will normalize and act as a headwind. EBIT margin expansion of 60 bps will be led by operating efficiencies and rupee depreciation. Expect muted net profit growth due to US$25 mn forex loss. We forecast net new deal wins of US$1.1 bn, flat qoq and up 38% yoy. Orange deal signed is substantial. Deal momentum in other verticals is also strong. Focus will be on the medium-term targets after it seems that the company may achieve EBIT margin and growth target for FY2027E. We expect investor focus on: (1) the path chosen by the company—do they expand margins further or reinvest to accelerate revenue growth, (2) the agentic AI approach of TechM, details of which are light at the moment, (3) performance in the underperforming financial services vertical, (4) profitability of the recently won large deals and (5) hedging strategy—the company has been reducing forward cover over the past few quarters. |