MPC Meet: RBI to maintain Status Quo against volatile backdrop; Policy In Uncertain Times: More Of An Art With A Dash For Scientific Outcomes

FinTech BizNews Service

Mumbai, April 6, 2026: As a prelude to MPC Meeting, taking place from April 6 to 8, 2026, the State Bank of India’s Economic Research Department has come out with a special research report, authored by Dr. Soumya Kanti Ghosh, Group Chief Economic Adviser, State Bank of India.

Since the last policy, a war raging in West Asia has plunged the entire world into chaos

❑ The de facto closure of the Strait of Hormuz and damage to regional infrastructure have produced the largest disruption to the global oil market in its history since 1973 according to the International Energy Agency

❑ Obviously, India is not unscathed from the current crisis and feeling the mercury rising. Rupee is already hovering above 93 per dollar and crude oil is adamant above $100/bbl resulting in jump in imported inflation across states. This along with projection of ‘Super El Niño’ may put upward pressure on inflation

❑ Alarmed over the spike in rupee’s gravitational pull during the current conflict, RBI has come out with several announcements, targeting curbing of speculations spread across both Onshore, as also Offshore NDF markets. However, some of the norms may pose operational challenges for Banks

❑ As the first policy since the staring of war, RBI would be much careful in communicating its position • As the situation is still evolving, we expect RBI to maintain status quo in the upcoming policy • Focus on addressing market microstructure: RBI needs to concomitantly explore the probability of conducting Operation Twist that pushes up the short-term yield while sobering the yield on long term papers ensuring various reference rates remain within the prescribed bands, aligned with policy rate in calibrated manner • Addressing balance of payment deficit through well crafted measures.

How has war impacted the entire WORLD?

Global economy is moderating due to trade wars, geopolitics and uncertainty.

Global GDP growth forecast have not seen revisions so far, but downward revision seems imminent

✓ S&P has revised its global growth outlook with European outlook seeing most of the downward revisions

✓ India’s growth for FY27 is forecasted at 7.2%

✓ Overall Global growth pegged at 3.2% (OECD, 2.9%)

✓ IMF going to publish its full assessment of world economy on 14 April

❑ Inflation is projected to increase and the pass through of higher energy and metal prices reflect in prices

✓ Stagflation risk is higher in 2026 if war prolongs

✓ G20 inflation projected 1.2% higher by OECD.

Broader rate cut trends show dominating preference for a pause

Central banks continue to revise their expectations on inflation after war in Middle East lingering ❑ Rate cuts dominate hikes so far, but the situation may change going ahead

On an average only 7 ships passing from Strait of Hormuz now down from 84

INDIA MACROS

Highest FII outflow since 1991

FY26 exhibited highest FII outflows at $16.6 billion since 1991

❑ Mar’26 outflows of $13.6 billion are highest after Mar’20 ($15.9 billion)

Rupee under pressure + Higher Crude oil prices

❑ Rupee after crossing the 90-mark slided rapidly

❑ In just 114 days, Rupee depreciated by Rs 3 per dollar Source: RBI; SBI Research; https://www.imf.org/en/blogs/articles/2026/03/30/how-the-war-inthe-middle-east-is-affecting-energy-trade-and-finance

❑ Oil and natural gas prices have increased significantly since the war began. Some markets for oil products have also been particularly affected, including those for diesel and jet fuel, whose benchmark prices have more than doubled in Asia (having higher Hormuz dependence)

making imported inflation a cause of worry…CPI FY27 numbers could have an upward bias..

❑ Exchange rate fluctuations and external shocks like supply chain disruptions, imported inflation (84 items, weight: 26.4%) is already at 5.4% (215 bps more than the headline) for Feb’26 and is expected to increase considerably further

❑ Consequently, CPI trajectory (as of now) may indicate more than 4.5% inflation for the next 3 quarters….though the FY27 projections are well under RBI’s target range

❑ However, Government’s recent decision for full customs duty exemption on a wide range of critical petrochemical products till June 30, 2026 may lower input costs and hence may have benign impact on imported inflation

….With some states will be impacted more

India Headline CPI: 3.21%. India Imported CPI: 5.36%

Based on the selected items we have calculated the state-wise imported inflation to understand how the current global situation may impact states’ imported inflation Except a few states (like WB, Punjab, Nagaland, etc.) all other states have greater imported inflation compared to overall inflation….Even more than 6% in MP, UP, AP, Rajasthan, TN.

Rupee depreciation clearly indicate spike in imported inflation

Interestingly, in Jan’26, Rupee depreciated by 2.35% m-o-m (highest monthly depreciation since Sep’22) which is clearly reflected in greater intensity in Red colour In Mar’26 rupee depreciated by 4.24% m-o-m and hence we expect a significant spike in imported inflation

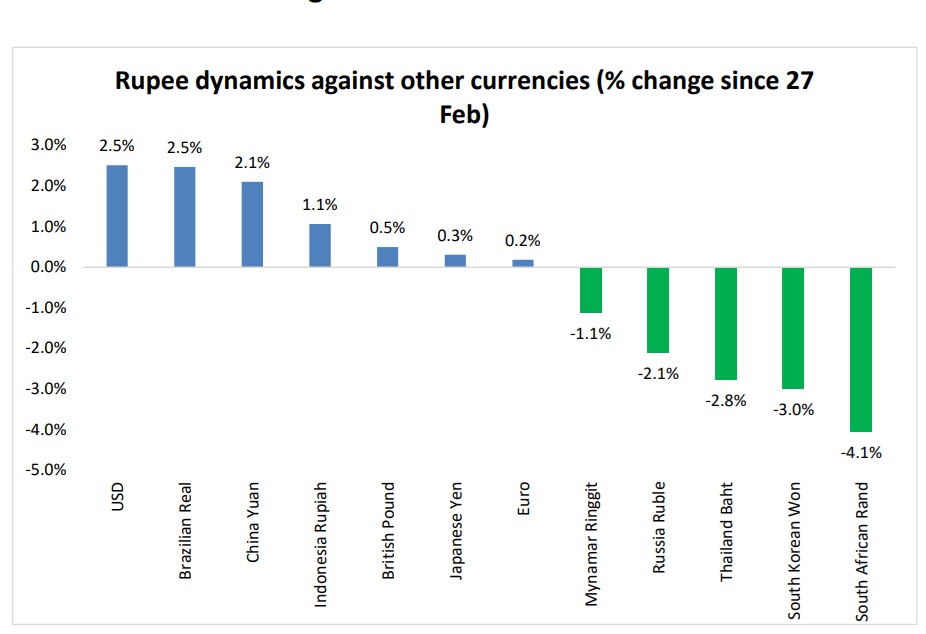

However, Rupee has appreciated against currencies of many emerging market economies since the beginning of the West Asia conflict

❑ Indian Rupee has depreciated against the dollar but clearly it is not the most impacted

❑ Rupee has appreciated against South African Rand, South Korean Won, Thailand Baht, Russian Ruble, Myanmar Ringgit. Even the depreciation against the Euro is not significant

A ‘Super El Niño*’ this year may spoil the Monsoon Party

❑ The current La Niña weather pattern is expected to ease this spring, and the El Niño pattern is projected to start building in the early summer (62% chance of El Niño developing between June and August)

❑ This year’s potential El Niño will be a ‘super’ version (when the ocean temperatures get much warmer than normal — 2 degrees Celsius above long-term average temperatures — it’s known as a “super El Niño”)

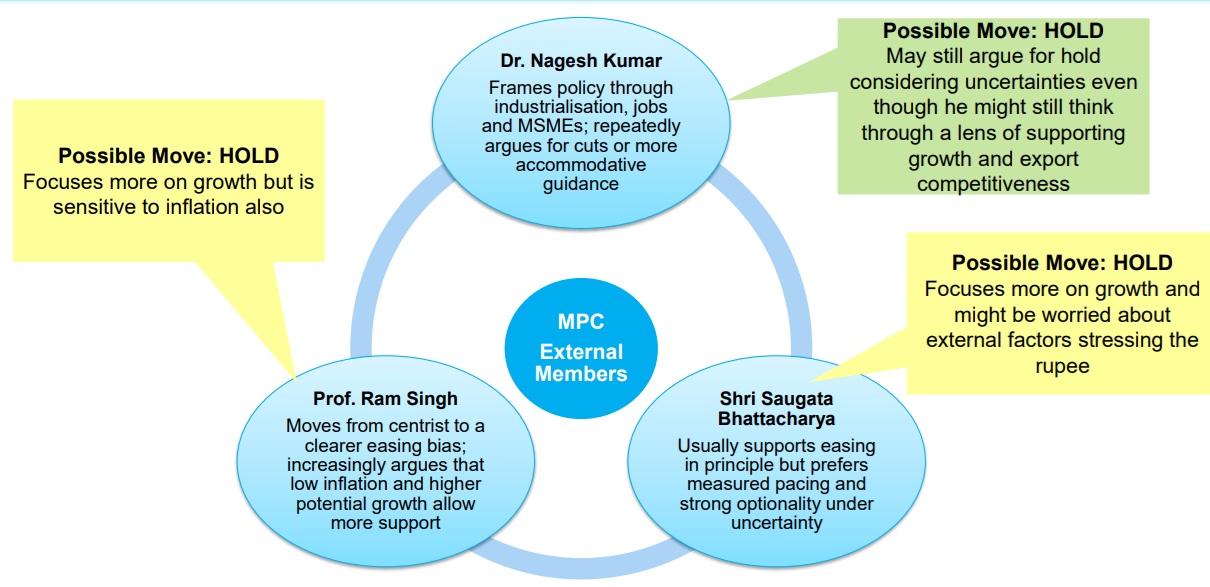

This MPC discussion are expected to be very different from the last… Can decision also be different?....

❑ Continuing to our earlier detailed discussion on MPC minutes…here we plot the similarity of MPC minutes vis-à-vis previous meeting

❑ A crisis or a composition change may alter the discussion, but will it lead to change in rates also???….Not really

Archetype of MPC Ext. Members & their possible reaction…Expecting a fractured decision

WHAT COULD THE RBI DO?

Liquidity should be modulated, RBI should focus on correcting market microstructure

❑ Surplus system liquidity has reduced from Rs 2.6 lakh crore in Feb 2026 to Rs 1.7 lakh crore in Mar 2026 ❑ Given the current volatility in rupee and yield, we believe the liquidity should be modulated to ensure rupee also gets support ❑ What is currently required is focus on correcting market microstructure. RBI needs to concomitantly explore the probability of conducting Operation Twist that pushes up the short-term yield while sobering the yield on long term papers ensuring various reference rates remain within the prescribed bands, aligned with policy rate in calibrated manner

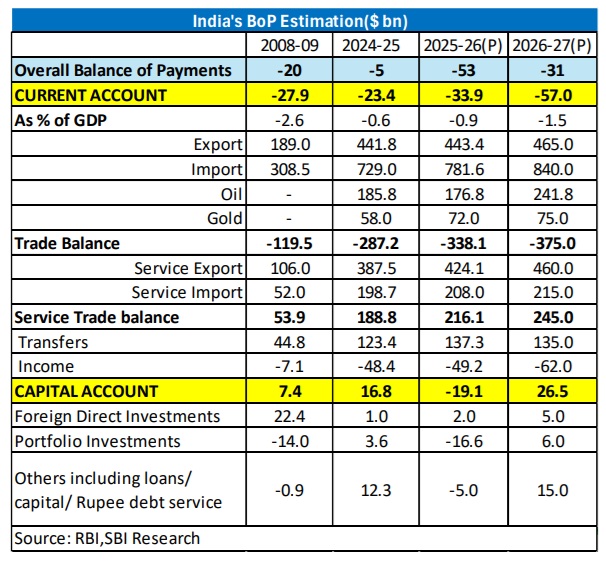

BoP to remain negative in FY27…

India needs a comprehensive package!

❑ Overall BOP projected to be in negative territory in FY27 (-$31 bn) with trade balance projected to be negative as well

❑ The capital account is projected to be in surplus of $26.5 bn on the assumption of positive flows next year

❑ Thus, a comprehensive measure is required given that BoP has been negative for the third consecutive year

Is a Non-Resident Driven Deposit Scheme Desirable at this Juncture?

❑ The strain on BoP front has front loaded the question of launching a Deposit mobilization scheme reminiscent of 2013, while also evoking success of RIB (1998) and IMD(2000) that had amassed sizeable flows in times of duress

❑ However, factoring the realities of yield curves across DMs (and its decoupling from policy rates), any such scheme needs to weigh in all the possible ‘what if’ scenarios on cost of funds (on resource mobilization front), hedging cost structure and lending costs for borrowers vis-à-vis opportunity costs

❑ Basis initial estimates, a 3 year foreign currency deposit sourced at say around 6.5-7.0% yield (sufficiently enticing for targeted investors to lock in funds), post hedging cost of 3 years, may spike to early double digits at lending table, check mating the very desirability of such funds at the end user level

❑ Also, the fact that in 2013, the super low effective cost of funds across DMs (yields in US were sub-1% for matching durations) had created a ‘virtuous’ leverage cycle wherein many Financial Institutions outside India had provided loans ballooning own corpus of depositors, with post credit cost (paid to FIs) return of such depositors-investors inching around 8-10%, creating a carry trade like situation…. The upheavals in most financial centers is restrictive of such practices (from both yields as also risks perspective) and hence depositors need a strong passionate emotional connect for anchoring the Viksit Bharat narrative as also exciting returns

❑ While a scheme soliciting funds is definitely workable that may also be designed to showcase the connect of the large diaspora spread globally and driving the innovation bandwagon, it has to be calibrated suitably across Corpus (a smaller corpus may entice higher demands while signaling no panic), yield (optimal from deployment angle too), tenor (no Hot money) and tax friendly treatment for investors

RBI recent measures to Support Rupee may be operationally challenging for Banks

❑ Alarmed over the spike in rupee’s gravitational pull during the current conflict, RBI has come out with a number of announcements, targeting curbing of speculations spread across both Onshore, as also Offshore NDF markets ❑ Over the years the NDF markets have become the force du jour providing directions to the domestic currency, with INR seemingly most reactive of the EM currencies pack through H2’2005 onwards

❑ While Offshore NDF markets have been the playground of major global Banks and trading entities (say hedge funds / large currency arbitrageurs) with substantial volume, the Onshore market has been the battle ground of domestic Banks / local traders, as also genuine protection seekers to hedge their exposure (given its cost advantage and ability to settle only the difference accruing on settlement)

❑ At the time of these instructions, total market O/S was estimated to be $45 Bn, with Banks having close to 3/4 th of the pie. Majority of positions are concentrated close to one month tenor; with 15-20% stretching beyond. Interestingly, PSBs are believed to not hold much positions beyond one month (or quite minimal), whereas other Banks generally have varying exposure across the curve (more risk-on sentiments evident with a rewarding compensation structure)

❑ Valuation curves for onshore and offshore trades are separate and regulator’s intent seems to be convergence of the two. However, given the short time horizon and spirit of instructions likely to cover entire Bank wide positions, these banks are likely to face significant M2M losses on NDF positions as they strive to square off their exposures

❑ The first series of measures targeted Banks’ open position (NOOP), curtailing Bank wide (and not trading book wide) open positions to $100 mn uniformly, with a deadline of April’10…interestingly, the straight jacket fixation of $100 mn limit for all categories of Banks, and uniformly applicable across banking / proprietary / order driven positions can be creating operational challenges for most Banks

RBI Measures to Support Rupee may be operationally challenging for Banks

❑ Close on the heels, second wave of regulatory orders issued on the first day of current FY attempt to plug the gap on deliverable forwards, limiting customer driven orders that have a speculative connotation while segregating the needful hedging purposes that REs can undertake post meaningful scrutiny of underlying exposures

❑ While the measures are reminiscent of 2013 (in particular if the OMCs are provided a separate window to meet their daily fx purchase needs), some flexibility to customers / REs in particular against the backdrop of increased trade / payment / settlement uncertainty wherein regulator has previously extended the window to 450 days, can ensure the framework retains genuine hedging requirements (what they are designed to be; a dynamic risk management tool and not some one time plaid static commitment, that may ultimately affect customers’ maneuverability more).

❑ Given NDF markets started as a hedging marketplace in the 80s for EMs that had little capital account convertibility by lenders having significant exposure, the moves by the regulator to deter Financial Institutions from placing lop sided speculative bets that anchor the free fall of rupee, can hardly be debated… yet, the limit need not be scale agnostic for all Banks, but should strive to balance the genuine requirements of the banking books and customer driven orders, separating the same from the trading book even as NOOP deadline closes in.