The system-level financial parameters of Scheduled Commercial Banks (SCBs) & NBFCs continue to be robust & sound

FinTech BizNews Service

Mumbai, June 6, 2025: The Monetary Policy Committee (MPC) held its 55th meeting from June 4 to 6, 2025 under the chairmanship of Shri Sanjay Malhotra, Governor, Reserve Bank of India. Sanjay Malhotra's statement, issued today after the MPC meet, is as follows:

The 55th meeting of the Monetary Policy Committee (MPC) was held in the backdrop of an early and promising start of the monsoon season, which is of vital significance for the Indian economy. In contrast, the global backdrop remains fragile and highly fluid. The uncertainty around the global economic outlook has somewhat ebbed since the MPC met in April in the wake of temporary tariff reprieve and optimism around trade negotiations. However, it is still high to weaken sentiments and lower global growth prospects. Accordingly, global growth and trade projections have been revised downwards by multilateral agencies.1 Moreover, the last mile of disinflation is turning out to be more protracted. As growth-inflation trade-off is becoming more challenging, monetary authorities are charting out a more cautious and carefully calibrated policy trajectory.

2. Looking beyond the near-term, growing economic and financial fragmentation is reshaping the global economy. Besides, complex interconnections within the financial system, elevated debt levels and growing influence of frontier technologies are raising financial stability concerns. Amidst heightened volatility in capital flows and exchange rates, coupled with constrained policy space, central banks of emerging market economies have a tougher task to stabilise their economies against global spillovers.

3. In this global milieu, the Indian economy presents a picture of strength, stability, and opportunity. First, strength comes from the strong balance sheets of the five major sectors - corporates, banks, households, government, and the external sector. Second, there is stability on all three fronts – price, financial, and political – providing policy and economic certainty in this dynamically evolving global economic order. Third, the Indian economy offers immense opportunities to investors through 3Ds – demography, digitalisation and domestic demand.2 This 5x3x3 matrix of fundamentals provides the necessary core strength to cushion the Indian economy against global spillovers and propel it to grow at a faster pace.

Decisions of the Monetary Policy Committee (MPC)

4. The Monetary Policy Committee (MPC) met on the 4th, 5th and 6th of June to deliberate and decide on the policy repo rate. After a detailed assessment of the evolving macroeconomic and financial developments and the outlook, the MPC decided to reduce the policy repo rate under the liquidity adjustment facility (LAF) by 50 basis points to 5.50 per cent with immediate effect; consequently, the standing deposit facility (SDF) rate shall stand adjusted to 5.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate to 5.75 per cent.

5. I shall now briefly set out the rationale for these decisions. Inflation has softened significantly over the last six months from above the tolerance band in October 2024 to well below the target with signs of a broad-based moderation. The near-term and medium-term outlook now gives us the confidence of not only a durable alignment of headline inflation with the target of 4 per cent, as exuded in the last meeting but also the belief that during the year, it is likely to undershoot the target at the margin. While food inflation outlook remains soft, core inflation is expected to remain benign with easing of international commodity prices in line with the anticipated global growth slowdown. The inflation outlook for the year is being revised downwards from the earlier forecast of 4.0 per cent to 3.7 per cent. Growth, on the other hand, remains lower than our aspirations amidst challenging global environment and heightened uncertainty.

6. Thus, it is imperative to continue to stimulate domestic private consumption and investment through policy levers to step up the growth momentum. This changed growth-inflation dynamics calls for not only continuing with the policy easing but also frontloading the rate cuts to support growth. Accordingly, the MPC voted to reduce the policy repo rate by 50 basis points to 5.50 per cent.

7. After having reduced the policy repo rate by 100 bps in quick succession since February 2025, under the current circumstances, monetary policy is left with very limited space to support growth. Hence, the MPC also decided to change the stance from accommodative to neutral. From here onwards, the MPC will be carefully assessing the incoming data and the evolving outlook to chart out the future course of monetary policy in order to strike the right growth-inflation balance. The fast-changing global economic situation too necessitates continuous monitoring and assessment of the evolving macroeconomic outlook.

Assessment of Growth and Inflation

Growth

8. The provisional estimates released by the National Statistical Office (NSO) placed India’s real GDP growth in 2024-25 at 6.5 per cent.3 During 2025-26 so far, domestic economic activity has exhibited resilience. Agriculture sector remains strong. With a very good harvest in both the kharif as well as rabi cropping seasons, the supply of major food crops is comfortable.4 The reservoir levels remain healthy.5 The highest procurement of wheat6 in the last four years provides a comforting stock position.7 Industrial activity is gaining gradually, even though the pace of recovery is uneven.8 Services sector is expected to maintain momentum.9 PMI services stood strong at 58.8 in May 2025, indicating robust expansion in activity.10

9. On the demand side, private consumption, the mainstay of aggregate demand, remains healthy, with a gradual rise in discretionary spending.11 Rural demand12 remains steady, while urban demand13 is improving. Investment activity is reviving as reflected by high-frequency indicators.14 Merchandise exports recorded a strong growth in April 2025 after a lacklustre performance in the recent past.15 Non-oil, non-gold imports posted a double-digit growth, reflecting buoyant domestic demand conditions.16 Services exports continue on a strong growth trajectory.17

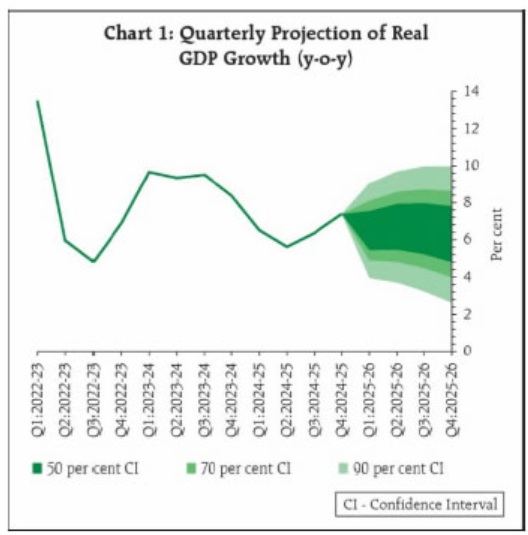

10. Going forward, the outlook for agriculture sector and rural demand is expected to receive further impetus by the expected above normal southwest monsoon rainfall.18 On the other hand, sustained buoyancy in services activity should nurture revival in urban consumption. The healthy balance sheets of banks and corporates; government’s continued thrust on capex;19 elevated capacity utilisation;20 improving business optimism21 and easing of financial conditions should help further revive investment activity. Trade policy uncertainty however continues to weigh on merchandise exports prospects, while conclusion of free trade agreement (FTA) with the United Kingdom22 and progress with other countries should provide a fillip to trade in goods and services. Spillovers emanating from protracted geopolitical tensions, and global trade and weather-related uncertainties pose downside risks to growth. Taking all these factors into consideration, real GDP growth for 2025-26 is projected at 6.5 per cent with Q1 at 6.5, Q2 at 6.7, Q3 at 6.6 and Q4 at 6.3 per cent. The risks are evenly balanced.

Inflation

11. CPI headline inflation continued its declining trajectory in March-April, with headline CPI inflation moderating to a nearly six-year low of 3.2 per cent (y-o-y) in April 2025. This was led mainly by food inflation, which recorded the sixth consecutive monthly decline. Fuel group witnessed a reversal of deflationary conditions and recorded positive inflation prints during March and April, partly reflecting the hike in LPG prices. Core23 inflation remained largely steady and contained during March-April, despite increase in gold prices exerting upward pressure.24

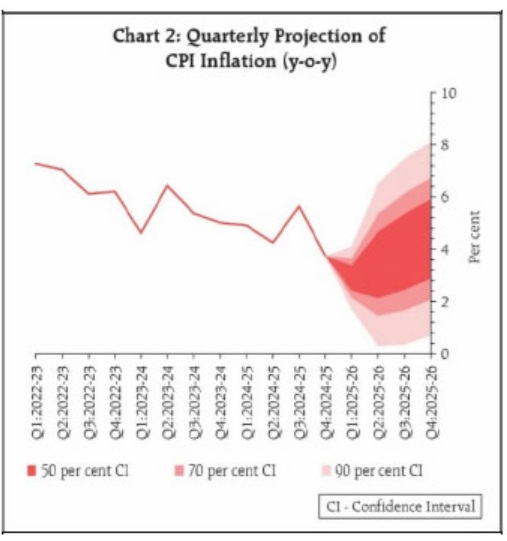

12. The outlook for inflation points towards benign prices across major constituents. The record wheat production and higher production of key pulses in the Rabi crop season should ensure adequate supply of key food items. Going forward, the likely above normal monsoon along with its early onset augurs well for Kharif crop prospects. Reflecting this, inflation expectations are showing a moderating trend, more so for the rural households.25 Most projections point towards continued moderation in the prices of key commodities, including crude oil. Notwithstanding these favourable prognoses, we need to remain watchful of weather-related uncertainties and still evolving tariff related concerns with their attendant impact on global commodity prices. Taking all these factors into consideration, and assuming a normal monsoon, CPI inflation for the financial year 2025-26 is now projected at 3.7 per cent, with Q1 at 2.9 per cent; Q2 at 3.4 per cent; Q3 at 3.9 per cent; and Q4 at 4.4 per cent. The risks are evenly balanced.

External Sector

13. With the moderation in trade deficit in Q4:2024-25, alongside strong services exports26 and remittance receipts, the current account deficit (CAD) for 2024-25 is expected to remain low.27 Furthermore, despite rising geopolitical uncertainties and trade tensions, India’s merchandise trade remained robust in April 2025. As imports grew faster than exports, trade deficit however widened during the month.28 Going forward, net services and remittance receipts are likely to remain in surplus, counterbalancing the rise in trade deficit. The CAD for 2025-26 is expected to remain well within the sustainable level.

14. On the financing side in 2024-25, foreign portfolio investment (FPI) to India dropped sharply to 1.7 billion US$, as foreign portfolio investors booked profits in equities.29 Net foreign direct investment (FDI)30 too moderated. It is germane to point out that this moderation is on account of a rise in repatriation and net outward FDI while gross FDI actually increased by 14 per cent. Rise in repatriation is a sign of a mature market where foreign investors can enter and exit smoothly, while high gross FDI indicates that India continues to remain an attractive investment destination. External commercial borrowings (ECBs) and non-resident deposits, on the other hand, witnessed higher net inflows compared to the previous year.31 As on May 30, 2025, India’s foreign exchange reserves stood at US$ 691.5 billion. These are sufficient to fund more than 11 months of goods imports32 and about 96 per cent of external debt outstanding.33 Overall, India’s external sector remains resilient as key external sector vulnerability indicators continue to improve.34 We remain confident of meeting our external financing requirements.

Liquidity and Financial Market Conditions

15. A total amount of ₹9.5 lakh crore of durable liquidity was injected into the banking system since January. As a result, after remaining in deficit since mid-December, liquidity conditions transitioned to surplus at the end of March. This is also evident from the tepid response to daily VRR auctions and high SDF balances – the average daily balance during April-May amounted to ₹2.0 lakh crore.

16. Reflecting the improvement in liquidity conditions, the weighted average call rate (WACR) – the operating target of monetary policy – traded at the lower end of the LAF corridor since the last policy. The comfortable liquidity surplus in the banking system has further reinforced transmission of policy repo rate cuts to short term rates. However, we are yet to see a perceptible transmission in the credit market segment, though we must keep in mind that it happens with some lag.

17. The Reserve Bank remains committed to provide sufficient liquidity to the banking system. To further provide durable liquidity, it has been decided to reduce the cash reserve ratio (CRR) by 100 basis points (bps) to 3.0 per cent of net demand and time liabilities (NDTL) in a staggered manner during the course of the year. This reduction will be carried out in four equal tranches of 25 bps each with effect from the fortnights beginning September 6, October 4, November 1 and November 29, 2025. The cut in CRR would release primary liquidity of about ₹2.5 lakh crore to the banking system by December 2025. Besides providing durable liquidity, it will reduce the cost of funding of the banks, thereby helping in monetary policy transmission to the credit market. I would like to reiterate that we will continue to monitor the evolving liquidity and financial market conditions and proactively take further measures, as warranted.

Financial Stability

18. The system-level financial parameters of Scheduled Commercial Banks (SCBs) continue to be robust. The asset quality parameters, liquidity buffers and profitability parameters have shown further improvement. Credit Deposit ratio for the banking system at the end of December 2024 was at 81.84 per cent, broadly similar to a year ago. Similarly, the system-level parameters of NBFCs too are sound with comfortable capital position and improved GNPA ratios.

19. The stress witnessed earlier in retail segments like unsecured personal loans and credit card receivables portfolio has abated, while the stress in micro-finance segment is persisting. Banks and NBFCs active in these segments are already recalibrating their business models, strengthening their credit underwriting practices and stepping up their collection efforts to avoid any excessive build-up of risks on this front in future.

Concluding Remarks

20. On both inflation and growth fronts, the Indian economy is progressing well and broadly on expected lines. Strong macroeconomic fundamentals and benign inflation outlook provide space to monetary policy to support growth, while remaining consistent with the goal of price stability. As global environment remains uncertain, it has become even more important to focus on domestic growth amidst sustained price stability. Accordingly, today’s monetary policy actions should be seen as a step towards propelling growth to a higher aspirational trajectory.

21. Here, I would like to highlight that there is no tussle between price stability and growth in the medium and long term. Price stability preserves purchasing power, imparts certainty to households and businesses in their savings and investment decisions and ensures congenial interest rate and financial conditions, all of which foster consumption, investment and overall activity. Moreover, it is crucial for equitable growth and shared prosperity because its absence is disproportionately burdensome on the poor.

22. I must also add that while price stability is a necessary condition, it is not sufficient to ensure growth. A supportive policy environment is vital. This is even more important during periods of high uncertainties such as the current times. At the Reserve Bank, therefore, while price stability remains the focus of monetary policy, we are not oblivious to putting in place complementary monetary and credit policies and regulations that support growth and prosperity.

Thank you. Namaskar and Jai Hind.