A Decade of Audacious Dreams: Bolder, Bigger and Indeed Beautiful: MUDRA Loans Sanctioned crossed Rs 33 Trillion

FinTech BizNews Service

Mumbai, April 2, 2025: The renewed emphasis on building blocks of production, chiefly MSMEs (apart from agri/allied activities) as twin growth enablers has seen credit offtake to MSMEs more than trebling to Rs 27.25 lakh crore in FY24, from Rs 8.5 lakh cr in FY14 (& estimated to hover around Rs 30 lakh crore in FY25)... In priority sector, MSME credit stood at 19.3% of SCBs adjusted net bank credit (ANBC) in FY24, compared to 15.8% in FY14, according to a research report authored by Dr. Soumya Kanti Ghosh, Group Chief Economic Adviser, State Bank of India.

❑ Launched by the PM in 2015 with a vision of enabling transparent, barrier-free (nil collateral) and adequate access to finance for the grassroots,that ultimately became a lynchpin of entrepreneurial dreams for scores of millions, Micro Units Development and Refinancing Agency (MUDRA) has been the ubiquitous vector of transformative change in bringing a credit revolution, curating the policy approach and credit decisions

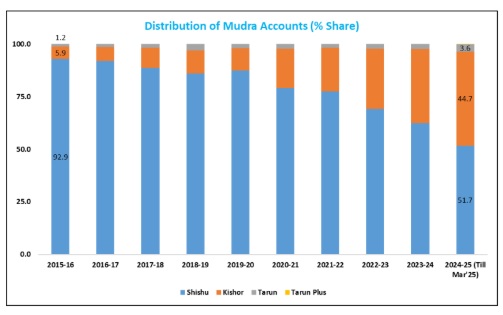

❑ During the decadal journey, cumulatively more than 52 crore accounts of MUDRA have been opened, of which 78% of the accounts are Shishu (40 crore), 20% are Kishor ( ~10 crore) and 2% Tarun/Tarun Plus (2 crore).... Interestingly, the share of Shishu in total accounts has declined from 93% in FY16 to ~51.7% in FY25, while the Kishor account share has increased to 44.7% in FY25 from a meagre 5.9% in FY16. This clearly indicates that many Shishu accounts have grown (natural progression) and availed Kishor loans of higher limit

❑ A kaleidoscopic view of the MUDRA landscape vouches the uber effectiveness across diversified intended beneficiary classes, raising the economic clout of the bottom the MOST as told by numbers... The growth in amount of loans disbursed averaged ~33% in the first three years. Again, disbursal increased by ~36% in FY23 signaling return of animal spirits at the bottom of the pyramid... also, average ticket size of the loans have shown maturity; ~Rs 1.02 lakh in FY25 from ~Rs 38,000 in FY16 indicating. A beacon of rising economies of scale and deepening of market depth/width

❑ The impact of PMMY on bringing the hitherto entrepreneurially devoid social groups is commendable, instilling a true sense of financial independence... close to half of the 52 crore PMMY accounts belongs to SC/ST and OBC social classes... Going a step further, 68% of total account holders are women entrepreneurs while 11% belongs to minority groups.

❑ Among states, Bihar has the largest number of PMMY women entrepreneurs (4.2 crore), followed by Tamil Nadu (4.0 crore) and West Bengal (3.7 crore)...Maharashtra has the largest share of women account holders (79%) in total followed by Jharkhand (75%) and West Bengal (73%)

❑ We strongly believe that increasing women participation in PMMY (68% of account holders are women) leads to better financial situation of women borrowers...In the last nine years (FY25 over FY16), while per woman PMMY disbursement amount increased by a CAGR of 13% to Rs 62,679, the per woman incremental deposits increased by a CAGR of 14% to Rs 95,269 branding PMMY an effective power tool for women empowerment at grass roots level

❑ Further, analyzing the UDYAM portal, Women-owned MSMEs constitute 20.5% of the total number of MSMEs registered on the portal since its inception on 1st July 2020. These women-owned MSMEs’ contribution to the employment generated by the total Udyam registered units is 18.73%. Thus, women-led MSMEs not only contribute to output generation but also to gender inclusivity.....State wise data reveals that Tamil Nadu has highest employment generation (15.7%) in women-led MSMEs followed by Maharashtra (12.1%) , Karnataka and Uttar Pradesh (8%). Thus, financial inclusion programmes like PMMY are pivotal in empowering women-led MSMEs

❑ States which have higher share of disbursements to women have significantly shown higher employment creation by women-led MSMEs further reinforcing the efficacy of targeted financial inclusion policies in fostering economic empowerment and labour market participation

❑ The impact of Mudra on financial inclusion across states (if states at lower quantiles of financial inclusion benefit differently from Mudra disbursements—especially those targeted at minorities and women—compared to states at higher quantiles), through a financial inclusion metric show Mudra disbursements have a stronger impact on states with lower financial inclusion levels...Mudra disbursements are benefiting financially weaker regions more, improving financial inclusion in underdeveloped states rapidly leading to convergence.... states that are less financially included receive proportionately greater benefits from the scheme, in a self-fulfilling prophecy

❑ Our analysis shows that while the overall diversity (entropy) of Mudra disbursements has become more skewed, but this skewness reflects a positive structural shift: the proportions allocated to developed regions has declined, while underdeveloped regions such as Bihar (from 5.67% to 10.97%), UP (from 9.27% to 11.30%), Odisha (from 4.24% to 4.51%) , and the North-East have experienced significant gains..... demonstrating a strategic reorientation of the Mudra scheme towards regions that need it the most.

Way forward

❑ Going forward, we expect ‘digital first’ approach of NBFCs, e.g., utilisation of account aggregator framework, will help further in flow of credit to MSMEs

❑ This is expected to get a boost from the proposed unified lending interface (ULI). In the pilot of ULI, the average ticket size of loans disbursed to MSME is Rs 9 lakh, so this will reduce turn-around-time further in a cost- effective manner