For both private and public sector banks, sequentially Opex growth would slightly lag business growth.

Shivaji Thapliyal,

Head of Research (Overall) & Lead Sector Research Analyst

Yes Securities

Mumbai, July 3, 2026: Yes Securities has come out with a special research report on Banks, with their Q1 FY27 Earnings Preview:

Asset quality:

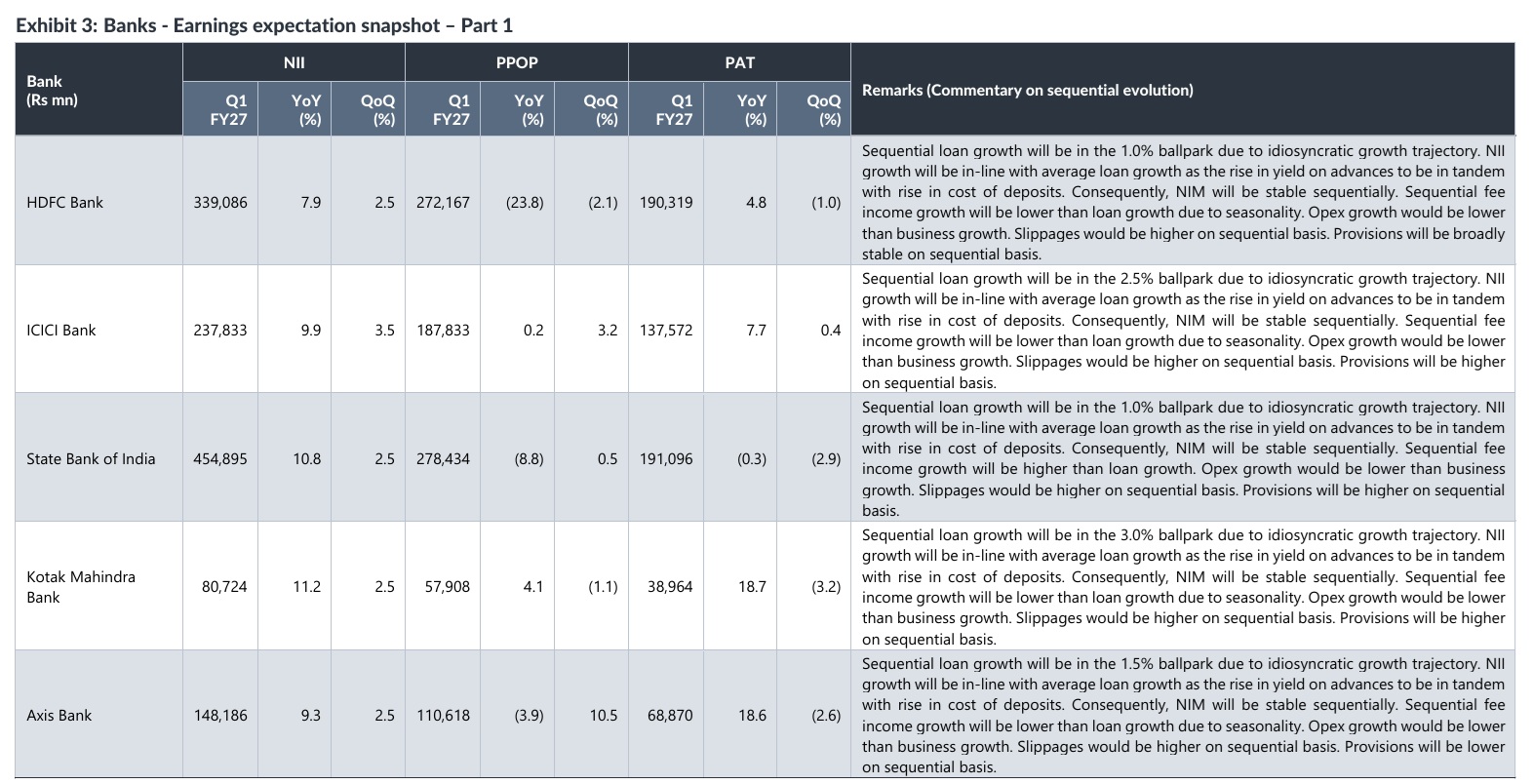

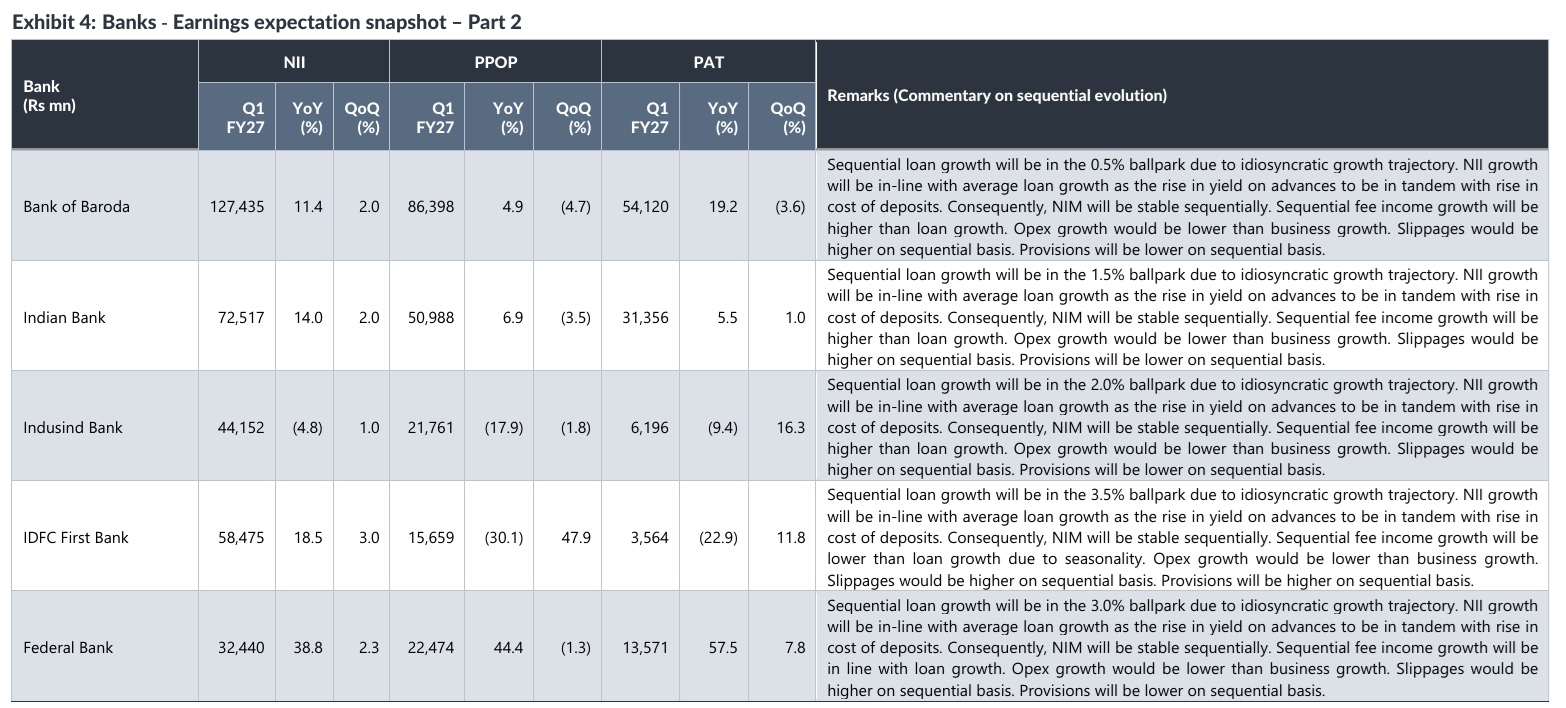

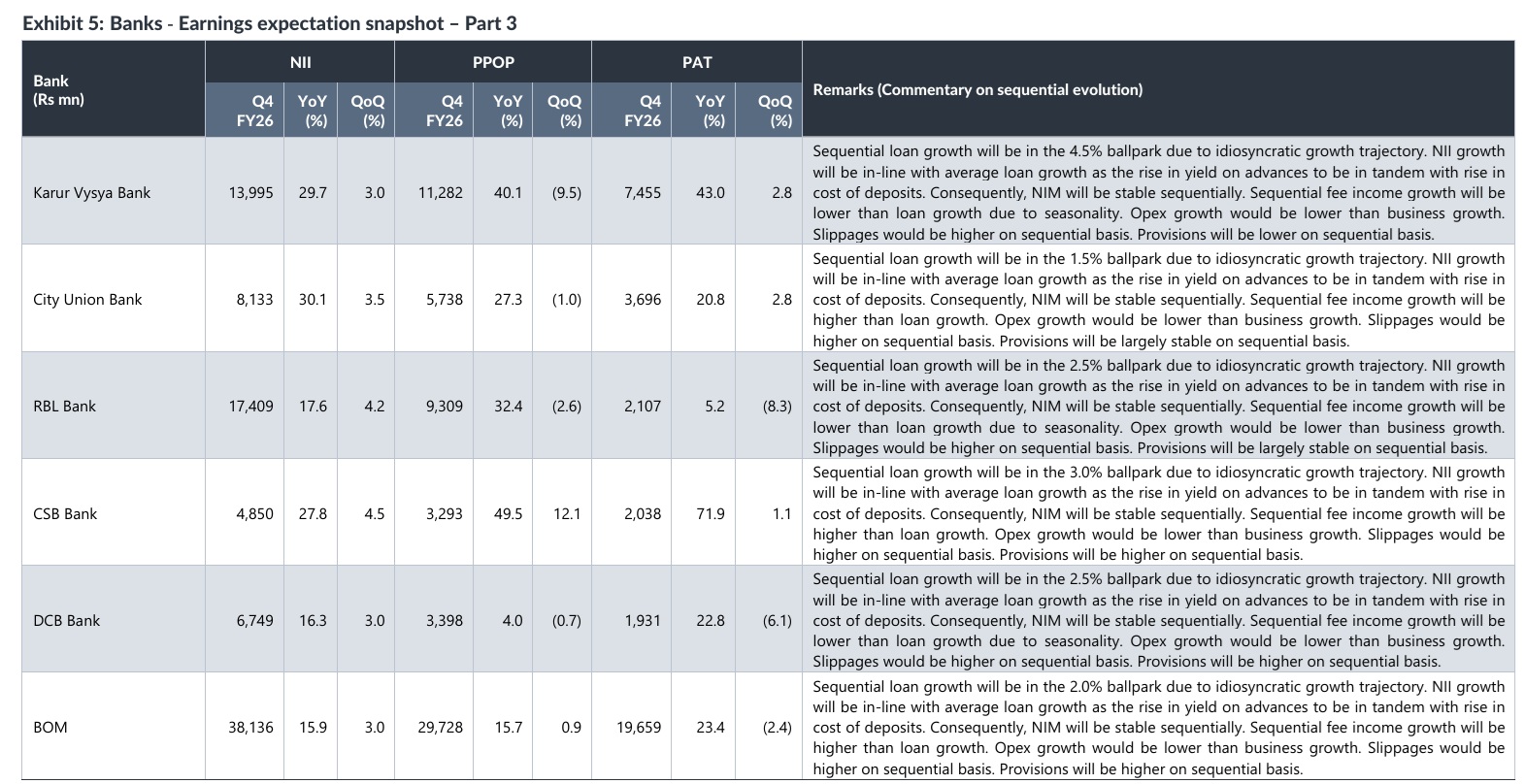

Fresh slippages in 1QFY27 are expected to be slightly higher on sequential basis on account of early impact from supply chain disruptions from the West Asia war, residual impact from tariff war and slow recovery in nominal GDP growth. Sequential evolution of provisions would be a function of not only slippages but also of one-offs in preceding quarters, ECL considerations and other idiosyncratic aspects. Hence, we see a sequential increase in provisions for ICICI, SBI, KMB, IDFCFB, CSB, DCB and BOM, a stable trend in provisions for HDFC, CUBK, and RBL whereas we expect sequential decrease in provision for AXSB, BOB, INBK, IIB, FB, and KVB.

Net interest margin:

All coverage banks are expected to report largely stable NIMs this quarter, sequentially. Not only has the impact from repo rate cuts played, the impact from MCLR reduction has also largely played out, with residual impact being offset by term deposit churn. Wholesale deposit cost has been brought under control with liquidity measures. The average Weighted Average Domestic Term Deposit Rate (WADTDR) for private sector banks for 2M1QFY27 declined -2 bps, to 6.69%, compared with the average for 4QFY26. The corresponding Weighted Average Lending Rate (WALR) was down by -4 bps to 9.89%, implying that Loan Spread inched lower by -2 bps for private sector banks. For PSU banks, the WADTDR fell around -8 bps to 6.63% and the WALR declined around -4 bps QoQ to 8.36%, which implies that Spread rose by 4 bps. It may be emphasized that the WADTDR and WALR for 2M1QFY27 excludes June month.

Loan growth

Sequential loan growth will be healthy (>4%) for KVB; moderate to reasonable (2.5-4%) for IDFCFB, CSB, FB, KMB, FED, RBK and DCB; sluggish to weak (<2.5%) for BOM, IIB, CUBK, AXSB, INBK, HDFC, SBI and BOB.

Opex growth: For both private and public sector banks, sequentially opex growth would slightly lag business growth.

Treasury profit:

The long-term bond yields have increased on sequential basis, with the 10-year yield averaging 6.96% over 1QFY27, higher by 25 bps QoQ. However, due to accounting for AFS book, there will be no MTM gain/loss on investment book but profits or losses actually booked will travel through the P&L The MTM gain/loss travels through the AFS reserve.