FICCI-IBA Bankers’ Survey (January - June 2024): NPA levels on a decline; Majority expect gross NPAs to be in the range of 2.5 - 3 per cent

FinTech BizNews Service

Mumbai, September 11, 2024: The nineteenth round of the FICCI-IBA survey was carried out for the period January to June 2024. A total of 22 banks including public sector, private sector and foreign banks participated in the survey. These banks together represent about 67 per cent of the banking industry, as classified by asset size.

The Indian economy and the banking sector remain robust and resilient. With improved balance sheets, banks are supporting economic activity through sustained credit expansion. However, credit growth is outpacing deposit growth, which could lead to liquidity challenges for the banking system. Raising deposits to keep pace with the loan growth and keeping the credit cost low remains on the top of banks’ agenda.

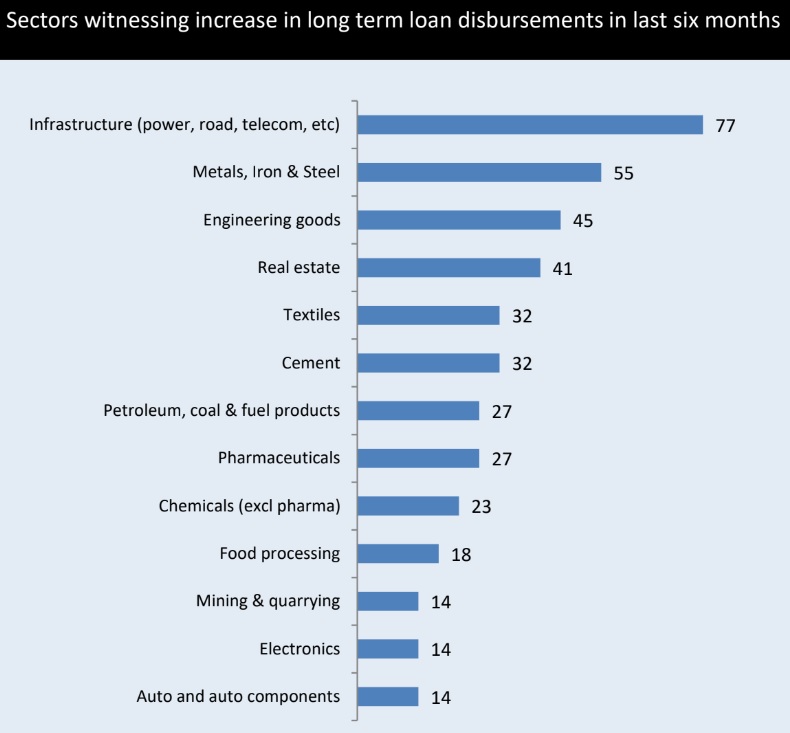

The survey findings show that long term credit demand has seen continued growth for sectors such as Infrastructure, Metals, Iron and Steel, Engineering. Infrastructure is witnessing an increase in credit flow with 77 per cent of the respondents indicating an increase in long-term loans. This could be attributable to the government’s capital expenditure push for the infrastructure sector. The survey suggests that the outlook on expectation for growth of non-food industry credit over the next six months is optimistic with 62 per cent of the participating banks expecting non-food industry credit growth to be above 12 per cent.

Customers’ search for higher-yielding investments and the ability to lock those interest rates for a longer time has led to a shift from low-cost to high-cost deposits, thereby increasing deposit costs for lenders. More than two-thirds of respondent banks (67 per cent) reported a decrease in the share of CASA deposits in total deposits in the current round of survey. Term deposits have picked up pace as reported by the respondent banks due to higher/attractive rates. 80 per cent of the participating Public Sector Banks reported a decrease in share of CASA deposits during the first half of 2024 while over half the private sector bank respondents reported a decrease in CASA deposits

In the current round of the survey, 68 per cent of respondent banks reported credit standards for large enterprises to have remained unchanged, largely similar as in the last round. Respondents reporting easing of credit standards has increased to 23 per cent in the current round as against 17 per cent in the previous round. For SMEs too, respondents reporting easing of credit standards has increased to 40 per cent in the current round as against 27 per cent in the previous round. 55 per cent of respondent banks reported credit standards for SMEs to have remained unchanged, as compared to 64 per cent in the last round.

In continuation with the trend witnessed in the previous round, a large majority (71 per cent) of the respondent banks reported a decrease in the NPA levels in the last six months. A significant 90% responding PSBs have cited a reduction in NPA levels while amongst participating Private sector banks, 67 per cent have cited a decrease. All the respondent Foreign banks cited no change in NPA levels over the last six months. Amongst the sectors that continue to show a high level of NPAs, most of the participating bankers identified sectors such as Textiles, Infrastructure and Food Processing.

Respondent banks continued to remain sanguine about the asset quality prospects in the current round of the survey, cushioned by policy and regulatory support and this was reflected in the survey results. Over half of the respondent banks in the current round believe that Gross NPAs would be in the range of 2.5 - 3 per cent over the next six months. 19 per cent respondents are of the view that NPA levels would be in the range of 2- 2.5 per cent. An overwhelming majority (70 per cent) of Public Sector respondents expect gross NPAs to be in the range of 2.5-3 per cent. 44 per cent of private bank respondents expect NPAs to be in the range of 2-2.5 per cent while all foreign bank respondents expect NPAs to be in the range of 2.5-3 per cent. As per respondents, some of the sectors that may continue to show NPAs over next six months include Agriculture, Textiles and garments, MSMEs, and Gems & Jewellery.

Resilient domestic economy accompanied by upgraded and improved credit assessment, effective and continuous credit monitoring, lower slippages, high write-offs and healthy capital position of banks were some of the key factors cited by respondent bankers who expect asset quality to further improve over the next six months.

The partnership between banks and fintech companies holds immense potential for driving innovation, improving service delivery, and enhancing financial inclusion. Respondent banks were asked to share their views and suggestions for strengthening this partnership. Some of the key suggestions provided by respondent banks related to seamless integration of technology, need for shared vision and customer centric approach, having effective communication, developing a robust governance framework for regulatory compliance and data security, co-creation of innovative solutions, and making investments in AI infrastructure.

Respondent banks were asked to share the measures taken by them in the realm of cyber-risk management. Banks shared specific measures taken by them in the areas of IT Governance and Risk Management, Cybersecurity Controls, Incident Response and Recovery, Vendor and External Risk Management. Respondent banks also shared the key strategies adopted by them to keep abreast with the skill requirements of the sector in current times. These included initiatives in the area of E- Learning, Coaching & Mentoring, Hackathons and Innovation Labs etc.

The Banks were also asked to provide inputs for making the ATM channel cost effective. The key suggestions offered include various measures to reduce operational expenditure, selecting strategic locations, increasing the interchange fees for ATM transactions, analysing costs and benefits for each ATM site, upgrading technology in ATMs, etc.