Provisions for Q3FY26 was Rs 810 crore (Rs 794 crore in Q3FY25 and Rs 947 crore in Q2FY26).

FinTech BizNews Service

Mumbai, 23 January 2026: The Board of Directors of Kotak Mahindra Bank (“the Bank”) approved the unaudited standalone and consolidated results for the quarter and nine-months ended December 31, 2025, at the Board meeting held in Hyderabad, today.

Consolidated results at a glance

Consolidated PAT for Q3FY26 stood at Rs 4,924 crore, up 5% YoY from Rs 4,701 crore in Q3FY25 (up 10% QoQ from Rs 4,468 crore in Q2FY26). Q3FY26 consolidated PAT includes estimated incremental cost of Rs 98 crore (post tax) pursuant to new Labour Code.

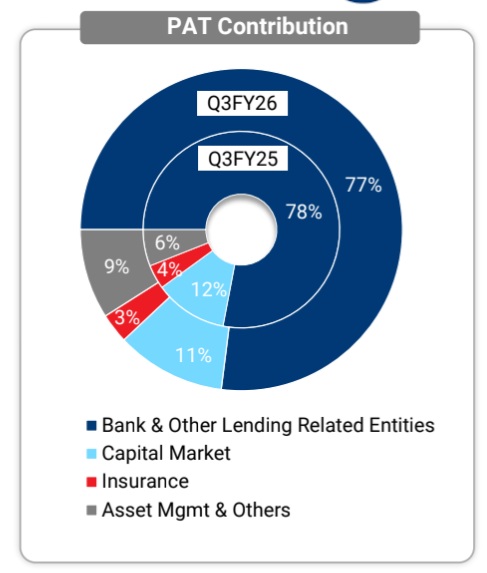

PAT of Bank and key subsidiaries given below:

PAT (Rs crore) | Q3FY26 | Q3FY25 | Q2FY26 |

Kotak Mahindra Bank | 3,446 | 3,305 | 3,253 |

Kotak Securities | 431 | 448 | 345 |

Kotak Asset Management & Trustee Company | 315 | 240 | 258 |

Kotak Mahindra Prime | 250 | 218 | 246 |

Kotak Mahindra Life Insurance | 162 | 164 | 49 |

Kotak Mahindra Capital Company | 98 | 94 | 60 |

Kotak Mahindra Investments | 87 | 107 | 120 |

Kotak Alternate Asset Managers | 75 | 10 | 104 |

Consolidated Customer Assets which comprise Advances (incl. IBPC & BRDS) and Credit Substitutes grew to Rs 598,780 crore as at December 31, 2025, up 15% YoY from Rs 519,126 crore as at December 31, 2024.

Total Customer Assets Under Management as at December 31, 2025 grew to Rs 787,950 crore, up 15% YoY from Rs 685,134 crore as at December 31, 2024. The total Domestic MF AUM increased by 20% YoY to Rs 586,610 crore as at December 31, 2025.

Consolidated Networth as at December 31, 2025 was Rs 175,251 crore. The Book Value per Share increased to Rs 176 as at December 31, 2025, up 15% YoY from Rs 154 as at December 31, 2024 (computed based on subdivision of 1 equity share of face value of Rs 5 each into 5 equity shares of Rs 1 each with effect from 14th January, 2026).

At the consolidated level, Return on Assets (ROA) for Q3FY26 (annualized) was 2.10%. Return on Equity (ROE) for Q3FY26 (annualized) was 11.39%.

Consolidated Capital Adequacy Ratio as per Basel III as at December 31, 2025 was 23.3% and CET I ratio was 22.4% (including unaudited profits).

Average Liqudity Coverage Ratio stood at 135% for Q3FY26.

Kotak Mahindra Bank standalone results

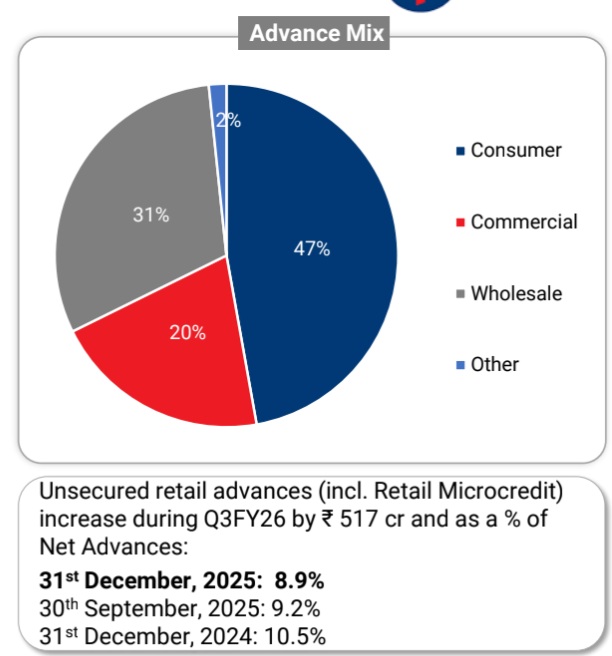

Net Advances increased 16% YoY to Rs 480,673 crore as at December 31, 2025 from Rs 413,839 crore as at December 31, 2024. Customer Assets which comprise Advances (incl. IBPC & BRDS) and Credit Substitutes grew to Rs 529,455 crore as at December 31, 2025, up 15% YoY from Rs 459,436 crore as at December 31, 2024

Total period-end Deposits grew to Rs 542,638 crore for Q3FY26, up 15% YoY from Rs 473,497 crore for Q3FY25.

Average Total Deposits grew to Rs 526,025 crore for Q3FY26, up 15% YoY from Rs 458,614 crore for Q3FY25. Average Current Deposits grew to Rs 75,596 crore for Q3FY26, up 14% YoY from Rs 66,589 crore for Q3FY25. Average Fixed rate Savings Deposits grew to Rs 118,505 crore for Q3FY26, up 12% YoY from Rs 105,682 crore for Q3FY25.

Average Term Deposits grew to Rs 318,070 crore for Q3FY26, up 19% YoY from Rs 267,743 crore for Q3FY25.

CASA ratio as at December 31, 2025 stood at 41.3%.

Cost of funds was 4.54% for Q3FY26 (5.06% for Q3FY25 and 4.70% for Q2FY26).

Credit to Deposit ratio as at December 31, 2025 stood at 88.6%.

Customers as on December 31, 2025 were 5.1 crore.

Net Interest Income (NII) for Q3FY26 increased to Rs 7,565 crore, up 5% YoY from Rs 7,196 crore in Q3FY25 (up 3% QoQ from Rs 7,311 crore in Q2FY26).

Net Interest Margin (NIM) was 4.54% for Q3FY26 (4.93% for Q3FY25 and 4.54% for Q2FY26).

Fees and services for Q3FY26 increased to Rs 2,549 crore, up 8% YoY from Rs 2,362 crore in Q3FY25 (up 6% QoQ from Rs 2,415 crore in Q2FY26).

Operating expenses for Q3FY26 increased to Rs 5,023 crore, up 8% YoY from Rs 4,638 crore in Q3FY25 (up 8% QoQ from Rs 4,632 crore in Q2FY26). Q3FY26 operating expenses include an estimated incremental cost of Rs 96 crore pursuant to new Labour Code. Excluding the impact of incremental cost due to new Labour Code, operating expenses for Q3FY26 were Rs 4,927 crore, up 6% YoY (up 6% QoQ). Cost to income was 48.3% for Q3FY26 which excluding the impact of incremental cost pursuant to new Labour Code was 47.4% for Q3FY26.

Operating profit for Q3FY26 increased to Rs 5,380 crore, up 4% YoY from Rs 5,181 crore in Q3FY25 (up 2% QoQ from Rs 5,268 crore in Q2FY26).

Provisions for Q3FY26 was Rs 810 crore (Rs 794 crore in Q3FY25 and Rs 947 crore in Q2FY26). Credit cost (annualised) for Q3FY26 stood at 0.63% (0.68% for Q3FY25 and 0.79% for Q2FY26).

The Bank’s PAT for Q3FY26 increased to Rs 3,446 crore, up 4% YoY from Rs 3,305 crore in Q3FY25 (up 6% QoQ from Rs 3,253 crore in Q2FY26).

As at December 31, 2025, GNPA was 1.30% & NNPA was 0.31% (GNPA was 1.50% & NNPA was 0.41% at December 31, 2024). As at December 31, 2025, Provision Coverage Ratio stood at 76%.

Standalone Return on Assets (ROA) for Q3FY26 (annualized) was 1.89%. Return on Equity (ROE) for Q3FY26 (annualised) was 10.68%.

Capital Adequacy Ratio of the Bank, as per Basel III, as at December 31, 2025 was 22.6% and CET1 ratio of 21.5% (including unaudited profits).