Steady Loan growth, tougher competition

FinTech BizNews Service

Mumbai, March 20, 2026: The latest Kotak Institutional Equities report focuses on banks:

Inexpensive banks, tougher trade-offs

We like large private banks in the current phase as the recent underperformance factors in the disappointment related to growth and return ratios. We find limited upside in regional banks, while public banks would find it challenging to replicate recent outperformance. Loan growth is steady amid rising competition and deposit constraints persist. Funding pressure and PSU pricing discipline skew private bank NIM risks to the downside.

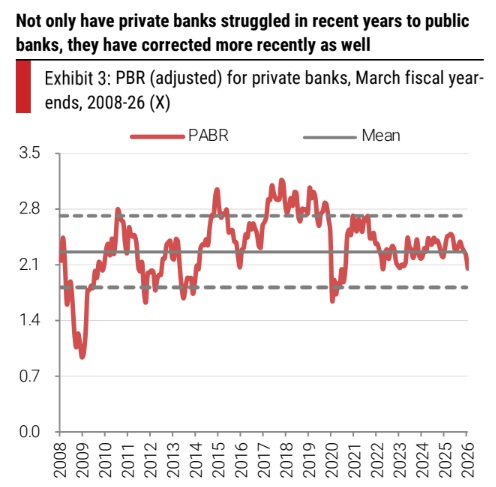

Indian banking valuations have moved into a more comfortable zone, driven by a de-rating in large private banks, while public sector banks have outperformed. Private banks now trade below long-term averages, whereas PSU banks are marginally above the historical average, compressing the valuation premium to levels closer to that of FY2010. While we find valuations attractive in large private banks, growth challenges persist and a recovery in industry-leading metrics is yet to become visible. We retain a negative view on regional banks due to stretched valuations. Unlike the past few years, we do not see meaningful pockets of inexpensive valuations at current levels. We expect similar returns in large banks (Axis, HDFC Bank and ICICI Bank). We like Bandhan Bank, DCB, Equitas and Ujjivan among mid/small banks. Among PSU banks, we do not expect any meaningful outperformance from SBI hereon.

Loan growth

Loan growth remains moderate at 12-14% yoy, below long-term averages, providing comfort from the portfolio risk. Corporate balance sheets remain conservatively positioned, with capex largely funded by internal accruals and limited drawdowns, supporting resilience amid global uncertainty. MSME credit continues to grow structurally faster, led by improved underwriting and data-driven analytics. Retail trends are mixed—housing growth moderated, auto loans remain resilient, unsecured lending slowed after earlier exuberance and gold loan growth has been strong—posing more risks to growth sustainability than asset quality. The competitive intensity has increased, with public banks gaining share in the lower-risk retail and granular segments. Lenders appear to be comfortable growing, despite a few headwinds on the horizon.

Funding stress and pressure on NIM remain key areas of concern

Deposit growth remains the binding constraint and trailing credit growth, with the gap increasingly funded by bulk/institutional deposits as household savings soften, reducing granularity and LCR usability. PSU banks have stopped ceding deposit market share and are now posting similar deposit/CASA growth as private banks, thereby compressing private banks’ traditional liability franchise edge. With limited visibility on a deposit upcycle, system deposit growth should stay in the low-to-mid teens. For private banks, this is a NIM-negative outcome—intensifying deposit competition lifts term deposit costs, while PSU banks’ lower RoE tolerance limits the transmission to loan-pricing, thereby presenting a downside risk to private banks’ NIM outlook.