ALL (NOT) QUIET AT THE WEST ASIAN FRONT

FinTech BizNews Service

Mumbai, April 10, 2026: With the MPC unanimously deciding to keep policy rate unchanged at 5.25%, while also continuing with the neutral stance, all eyes and ears naturally turned to the undertone and reading between the lines of the Governor statement even as ample indications of the MPC being in wait and watch stance in a flux like situation was self evident.

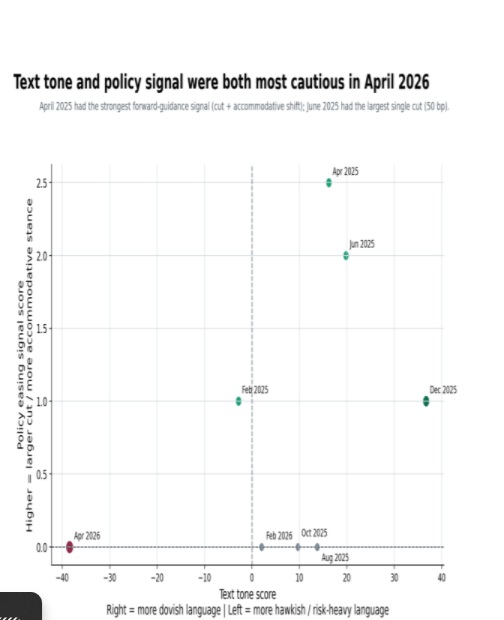

We quantified the information in the policy text using Natural Language processing techniques and created a dovish/ hawkish tone score using our custom made dictionary. Out of the eight statements by the current governor, this statement is most cautious/hawkish in our opinion but does not mean a rate hike is imminent. The choice of words and the latent signal the latest statement carries reflects deep understanding of the evolving geo-economic situation in the world without hinting at any imminent rate hike with regulatory gaze hobbling between growth and inflationary concerns.

Average inflation is projected at 4.6% for FY27, with core inflation is projected at 4.4% for FY27. As on date, RBI expects FY27 real GDP growth at 6.9% with progressive upgrades in second half of current fiscal. Further, volatility in crude oil and other commodity prices along-with possible El Niño conditions impart considerable volatility to inflation. However, the near -term food supply prospects have been boosted by robust rabi crop providing some comfort. RBI has also indicated that it will be actively intervening for managing liquidity .

On the regulatory and development front, the regulatory measures have largely focused on banking sector. The RBI has proposed to rationalize two guidelines that affect the capital planning of banks. The first proposal is to remove the rider on deviation in incremental NPA by 25% for taking quarterly profits in calculation of CRAR. This proposal gives considerable flexibility to banks to internal plough back. The second proposal is to dispense away with the requirement of investment fluctuation reserves (IFR). The IFR was additional reserve under Tier 2 to cover the losses on non-HTM investment book. With banks already covering these losses under capital charge for market risk and other income recognition provisions, IFR was a duplication in some sense. The proposal irons out this and makes risk recognition more transparent and simpler. Also, basis some rough back of the envelop calculations, Indian Commercial Banks can see the IFR corpus of around 35-40,000 crore getting freed up through reversal (@2.5 of HFT and FVTPL-AFS portfolios of around Rs 14 lakh cr book, presuming a straight jacketed ~20% of Banks investment book of around 70 lakh cr). This corpus can be used optimally and judiciously by Banks between CET-1 and P&L account even when yields have moved substantially up during last quarter.

To strengthen the governance by way of optimal utilization of time, it is proposed that board level activity governed by RBI directions will be rationalized with more strategic policy making and risk governance. That should make boards more attuned to screen evolving landscape dotted with risks, a prerequisite in these tumultuous non-linear times. On the supervision side, the RBI has further consolidated 64 Master Directions in nine functional areas thus reducing the compliance cost for banks. On the payment system side, it is proposed to dispense with the requirement of due diligence of MSMEs while onboarding on TReDS platforms. This measure is expected to further increase trading volumes on platform and offer liquidity to the sector. Banks and regulators would however need to identify risks inherent proactively on this front.

Finally, on the market development side, participant base of the term money market is proposed to be expanded to include non-bank participants viz., AIFIs, NBFCs, HFCs with enhanced limits for specified PDs. Since banks are net lenders, the move is positive as it expands the demand for funds and deployment of intraday surplus funds. This move is largely expected to have a sobering impact on yields going forward. Interestingly, as emphatically iterated by the Governor today, the rapid depreciation thrust upon the INR off late is not in sync with India’s macro fundamentals and a course correction was a much-needed recourse with currency now retreating towards its implied value, with a sledge hammer pounding from the Mint street paving the way. Similarly, for an emerging market, targeted fx intervention remains an absolute necessity.

Can we pitch the GIFT city as a credible alternative to global financial centers with less compliance and regulatory hurdles that dissuade the vicious loop and biases impacting downward outlook on rupee ?

Overall, we expect a prolonged pause as the natural outcome under current uncertain global environment.

MPC KEPT REPO RATE UNCHANGED AT 5.25%

MPC unanimously decided to keep repo rate unchanged at 5.25%. The MPC also continued with the neutral stance. MPC will wait and watch the changing circumstances before taking any decision on interest rates.

RBI expect FY27 real GDP growth at 6.9% (as compared to 7.6% growth in FY26) with Q1 at 6.8%; Q2 at 6.7%; Q3 at 7.0%; and Q4 at 7.2% owing to elevated energy and commodity prices coupled with supply shoch disruptions. While exports may be adversely impacted the growth, the services sector is in excellent shape.

Volatility in crude oil and other commodity prices alongwith possible El Niño conditions impart considerable volatility to inflation. However, the near-term food supply prospects have been boosted by robust rabi crop providing some comfort. Overall, RBI expect FY27 inflation at 4.6% with Q1 at 4.0%; Q2 at 4.4%; Q3 at 5.2%; and Q4 at 4.7%. Core inflation is projected at 4.4% for FY27. TONE OF GOVERNOR’S STATEMENT • The latest statement by the RBI governor is heaviest during his tenure in tone marked by the use of words like “uncertainty”, “risk”, “elevated energy prices”, “slowdown”, “shocks”, “disruptions”. This is the first instance of his tenure where a real supply side crisis has emerged. Our claim is borne out by a reading of the governor’s statement, use of words like “uncertainty”, “risk”, “elevated energy prices”, “slowdown”, “shocks”, “disruptions” signal caution on part of the central bank. Energy supply side shocks like this one are not manageable by monetary tools alone. So it is prudent on the part of the Reserve Bank to wait and let the situation unfold.

• ·To derive the tone of the policy, we quantified the information in the text using Natural Language processing techniques and created a dovish/hawkish tone score using our custom made dictionary that maps words into these two labels. Note here hawkish tone indicates caution not necessarily a rate hike.

• Our analysis indicated that the most dovish tone yet by the current governor was used in December 2025 statement, where inflation was low and geopolitical situation was not as unpredictable as it is now. Out of the eight statements by the current governor this statement is most cautious/hawkish in our opinion but does not mean a rate hike is imminent. The choice of words and the latent signal the latest statement carries reflects deep understanding of the evolving geo-economic situation in the world.

LIQUIDITY MANAGEMENT

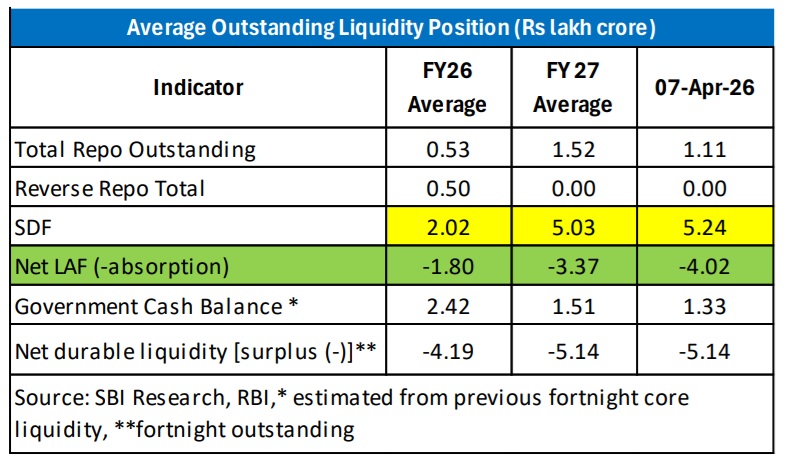

Liquidity surplus which moderated to Rs 1.7 lakh crore in Mar’26 from Rs 2.6 lakh crore in Feb’26, increased to Rs 3.4 lakh crore in April so far. RBI has been actively intervening for managing liquidity.

Since the last MPC meeting in Feb’26, RBI has injected Rs 4.6 lakh crore liquidity in the banking system, through OMO purchase of Rs 1 lakh crore and VRR of Rs 3.6 lakh crore of various tenures.

RBI in MPR April 2026 (pp 17) studied the ‘optimal Level of Liquidity’ and the findings suggests that surplus liquidity in the range of 0.6-1.1% of NDTL likely to keep the WACR below the repo rate between 5-10 bps, while liquidity deficit in the range of 0.4-0.7% of NDTL is likely to keep the WACR above the repo rate between 5 to 10 bps.

DEVELOPMENTAL AND REGULATORY POLICIES

a) NPA provisioning for inclusion of quarterly profits in CRAR computation: Basis extant instructions, a bank might reckon the profits in current financial year for CRAR calculation on a quarterly basis provided the incremental provisions made for NPAs at the end of any of the four quarters of the previous financial year had not deviated more than 25 per cent from the average of the four quarters, the impact being Banks were not able to utilize the quarterly profits for CRAR calculation during quarters. With current changes, Quarterly profits can be considered for CRAR calculation without any linkage to deviation in Loan Loss Provision thus henceforth, Banks will be able to consider the quarterly profits in CRAR calculation.

b) Dispensing with the requirement to maintain an Investment Fluctuation Reserve (IFR): RBI today announced dispensing with the requirement to maintain IFR (classified as Tier-II capital currently) as an additional buffer to hedge against depreciation in the value of investments, providing commercial Banks with manoeuvrability to optimally shift the duplicated provisions between Tier-I capital or P&L account through reversal.

• Incidentally, to ensure smooth transition to Basel II norms, banks were advised in June’2004 to maintain capital charge for market risk in a phased manner, building up IFR of a minimum 5% of the investment portfolio with a view to hold adequate reserves to guard against any possible reversal of interest rate environment in future due to unexpected developments.

Banks are understood to keep IFR in the range of 2- 3% of their non-HTM portfolio today. Keeping just 20% of investments in non-HTM category for SCBs (~14 lakh cr) and a 2.5% IRF, we understand a corpus of around ~35-40,000 cr can be reversed for Commercial Banks (internal adjustments).

c) RBI’s Proposal to Revise Board Governance Norms to bank board governance norms to enhance their focus on policy-level decision-making. The proposed changes aim to reduce board involvement in day-today operations and improve governance efficiency. This would allow boards to allocate more time to strategic and policy-related decisions. This may lead to improved corporate governance standards and reduced internal conflicts. The framework also aligns with global best practices in banking governance.

d) Consolidation of supervisory instructions: The draft supervisory Master Directions, now placed on the RBI’s website for public comments, consolidate existing instructions across key functional areas into a structured format. This is expected to improve consistency in inspections, reduce ambiguity in supervisory expectations, and align oversight more closely with the reworked regulatory framework. The move also signals a shift towards more structured and riskbased supervision. With clearer supervisory benchmarks, regulated entities are likely to gain better visibility into compliance expectations, enabling stronger governance and internal control systems.

• As with the earlier regulatory overhaul, the supervisory consolidation is not expected to materially change compliance requirements. Instead, it is aimed at improving transparency, reducing duplication, and making the overall regulatory ecosystem more navigable.

e) Simplifying the onboarding processes of MSMEs in TReDS: RBI has proposed easing on boarding norms for MSMEs on the Trade Receivables Discounting System (TReDS), in a move aimed at improving their access to timely working capital. The move is expected to reduce friction in the registration process and encourage more small businesses to participate in invoice discounting, a segment that remains underpenetrated despite policy support. f) Development of Term Money Market: For further development of the term money market, the regulator has broadened the perimeter of eligible entities, including now non-bank participants viz., AIFIs, NBFCs, HFC with enhanced borrowing limits for SPDs. We understand it is an important step that would deepen and broaden the G-Sec market, being yield accretive going forward.

OTHER MEASURES

• Retail Participation in Bond Market: At present, the retail participation (RBI Retail Direct) in bonds markets is meagre despite constant regulatory promotion of sovereign debt to households (~3.58 lakh accounts on date with Floating rate savings bond making 48% of total holdings). We understand enabling true dematerialization of Retail Direct holdings, a la equities, would promote interoperability and entice strong interest from retail investors which can make debt an attractive proposition for holding as also trading activities by a wider cohort.

• Remittances to increase in FY26 but will be stable in FY27: During FY26 (till Dec) India received remittances of $110 billion, compared to $100 billion during Apr-Dec’25. With the increased escalation in West Asia, we expect remittances to India may reach all time high of $137-140 billion in FY26 but will be in the range of $135-137 billion in FY27.

CREDIT GROWTH: BANKS VIS-À-VIS NBFCS

• Bank credit recorded a robust growth during second half of FY26, owing to monetary policy easing and strong economic activity. Bank credit grew by on an average 14.5% in the last three month (Dec’25 to Feb’26) due to robust growth in personal loans and services sector. Credit growth in the personal loans segment was driven primarily by housing loans, vehicle loans and loans against gold jewellery.

• While credit extended by NBFCs has also strengthened and growing in double digits since Sep’25 (3-month average: 13.9%), it is mainly driven by retail loans (which has share of 42.6% in overall credit). Further, as per RBI’s latest MPR, NBFCs are playing important role in providing formal credit to niche sectors in the economy in form of lending to infrastructure, especially power sector. It is notable to mention that while share of loans against gold jewellery plus consumer durables in the case of NPFCs is 6.3% it is 2.2% for banks.