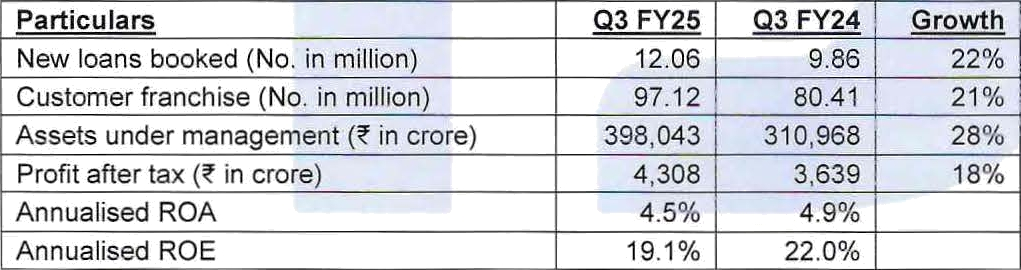

Number of new loans booked in Q3 FY25 was highest ever at 12.06 million as against 9.86 million in Q3 FY24, a growth of 22%.

FinTech BizNews Service

Mumbai, January 29, 2025: A meeting of the Board of Directors of Bajaj Finance Limited (BFL) was held today to consider and approve the

unaudited standalone and consolidated financial results for the quarter ended 31 December 2024.

Bajaj Finance reports: Financial results for Q3 FY25

Consolidated profit after tax of Rs4,308 crore for Q3 FY25

Consolidated assets under management of Rs398,043 crore as of 31 December 2024 Highest ever new loans booked of 12.06 million in Q3 FY25

Highest ever quarterly increase in customer franchise of 5.03 million in Q3 FY25.

The consolidated financial results include the results of BFL and following subsidiaries and associates:

Entity name |

voting power of BFL | Consolidated as | |

Bajaj Housin9 Finance Limited (BHFL) | 88.75’/" ’ | Subsidiary | |

Bajaj Financial Securities Limited (BFinsec) | 100°/ ! | Subsidiary | |

Snapwork Technologies Private Limited | 41.50"/” | Associate | |

Pennant Technologies Private Limited | 26.53°â* | Associate | |

°reduced front 100% to 88.75a? effective 13 September 2024 consequent to allotment of equity shares pursuant to

Initial Public Offer (IPO) ”on fully diluted basis

CONSOLIDATED PERFORMANCE HIGHLIGHTS

| Q3 FY25 | Q3 FY24 | Growth |

New loans booked (No. in million) | 12.06 | 9.86 | 22’/ |

Customer franchise (No. in million) | 97.12 | 80.41 | 21% |

Assets under management (7 in crore) | 398, 043 | 310,968 | 28°/ |

Profit after tax (7 in crore) | 4,308 | 3,639 | 18°% |

Annualised ROA | 4.5* ’ | 4.9% |

|

Annualised ROE | 19.1% | 22.0 |

|

CONSOLIDATED PERFORMANCE HIGHLIGHTS — Q3 FY25

Number of new loans booked in O3 FY25 was highest ever at 12.06 million as against 9.86 million in Q3

FY24, a growth of 22%.

Customer franchise stood at 97.12 million as of 31 December 2024 as compared to 80.41 million as of 31 December 2023, a growth of 21%. In Q3 FY25, the Company recorded highest ever quarterly increase in its customer franchise of 5.03 million.

Assets under management (AUM) grew by 28% to Rs 398, 043 crore as of 31 December 2024 from

Operating expenses to net total income for Q3 FY25 was 33.1% as against 33.9* in Q3 FY24.

Pre-provisioning operating profit increased by 27% in Q3 FY25 to Rs 7,805 crore from Rs 6,142 crore in Q3 FY24.

< Profit before tax increased by 18% in Q3 FY25 to Rs 5,765 crore from Rs 4,896 crore in Q3 FY24.

< Profit after tax increased by 18% in Q3 FY25 to Rs 4,308 crore from Rs 3,639 crore in Q3 FY24.

Gross NPA and Net NPA as of 31 December 2024 stood at 1.12% and 0.48* respectively, as against 0.95°/ and 0.37% as of 31 December 2023. The provisioning coverage ratio on stage 3 assets was 57%.

Capital adequacy ratio (CRAR) (including Tier-II capital) as of 31 December 2024 was 21.57%. The Tier-I

capital was 20. 79"/ .

The Company enjoys the highest credit rating of AAA/Stable for its long-term debt programme from CRISIL, ICRA, CARE and India Ratings, Al+ for short-term debt programme from CRISIL, ICRA, CARE and India Ratings and AAA (Stable) for its fixed deposits programme from CRISIL and ICRA.

The Company has been assigned long-term issuer rating of BBB-/Stable and short-term issuer rating of A-3 by S&P Global ratings. Also, the Company has been assigned Baa3/P-3 long-term and short term foreign and local currency issuer ratings with stable outlook by Moody's ratings.

Recently, the Company announced a strategic partnership with Bharti Airtel, one of India's largest telecom services providers. This partnership combines Airtel's highly engaged customer base of 375 million, strong distribution network of over 1.2 million, and Bajaj Finance's diversified suite of 26 product lines, distribution hell of 224K distribution points. its 4,259 locations and 70,000 field agents.

Airtel will offer Bajaj Finance's retail and MSME products on its Airtel Thanks App and its nation-wide network of stores in a seamless and secured manner. The combined strength of the companies’ digital assets will enable significant increase in penetration of financial products and services in India.

To start with, two products of Bajaj Finance have been piloted on the Airtel Thanks App. By March, nine products of Bajaj Finance will be available to customers on the Airtel Thanks App. BFL and Airtel will enable more products through FY26.

During Q3 FY25, the Company has mutually agreed to cease incremental sourcing of Co-Branded Credit Cards with RBL Bank Limited and DBS India Limited. This decision will not affect existing cardholders, who will contin ue to receive services from the respective banks as usual. The Company earned distribution fees and a revenue share under the co-brand arrangement The discontinuation will not impact the Company's future revenue share from this arrangement.

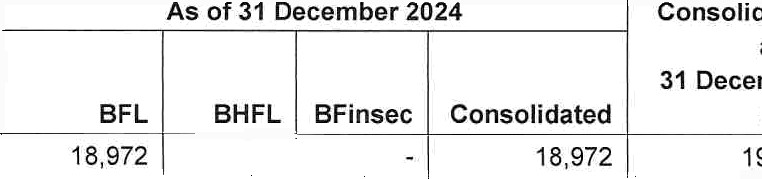

A — Breakup of consolidated AUM and deposits book

(Rs in crore)

AUM | As of 31 December 2024 Consolidated as of 31 December

| |||||||

Two & Three-Wheeler Finance | 18,972 |

| - |

| 18,972 | 19,384 | (2"%) | |

Urban Sales Finance | 29,149 |

|

|

| 29,149 | 24,485 | 19* | |

Urban B2C Loans | 81,533 | 1,610 | - |

| 83,143 | 61,705 | 35% | |

Rural Sales Finance | 7,955 | - | - |

| 7,955 | 6,166 | 29% | |

Rural B2C Loans | 20,135 | - | - |

| 20,135 | 17,405 | 16°% | |

Gold Loans | 7,267 | - | - |

| 7,267 | 4,021 | 81’/ | |

SME Lending |

| 116 |

|

| 46,943 | 35,738 | 31% | |

Car Loans |

| 11,141 | - l |

|

| 11,141 | 5,658 | 97% |

Conlmercial Lending |

| 26,449 | |

|

|

| 26.057 I | 20,672 | 26 ' |

Loan against securities | ! | 19,870 |

| 5,392 |

| 25,262 i | 19,205 | 32% |

Mortgages |

| 24,072 | 106,588 |

|

| 122,019 i | 96,529 | 26*1 |

Total AUM |

| 293,370 | 108,314 | 5,392 | t | 398,043, | 310,968 | 28% |

(Rs in crore)

|

Deposits |

| As

BFL | of | 31 December

BHFL | 2024

Consolidated | Consolidated as of 31 December 2023 |

Growth |

Deposits | 68,760 | 37 | 68,797 ! | 58,008 | 19*S | |||

Appd''xinJately 20*â of the c onsolidated burrov/ings and 27’/« of the standalone borrowings.

B - Summary of consolidated financial results

(Rs in crore | |||||

Particulars Q3’25 | o3‘24 | QoQ | 9M’25 9M'24 | 9Mo9M | FY24 |

New loans booked (No. in million) 12.06 | 9.86 | 22% | 32.72 28.33 | 15’/ | 3620 |

Assets under management 398,043 | 310,968 | 28* | 398,043 310,968 | 28’% | 330,615 |

Assets under finance 390,191 | 306,389 | 27% | 390,191 306,389 | 27% | 326,293 |

Interest income 15,768 | 12,523 | 26* | 44,804 35,077 | 28* | 48,307 |

Interest expenses 6,386 | 4,868 | 31% | 18,219 l 13,508 | 35°? | 18,725 |

Net interest income 9,382 | 7,655 | 23% | 26,585 21,569 | 23% | 29,582 |

Fees and commission income 1,511 | 1,291 | 17% | 4,461 3,943 | 13"% | 5,267 |

Net gain on fair value changes 165 | 68 | 143* | 416 230 | 81% | 308 |

Income on de-recognised loans 190 | 20 and Sale of services | 850* | 437 54 | 709* | 63 | |

Others* 425 ! 264 | 61% | 1.138 747 | 521S | 1,038 | |

Net total income 11,673 i 9,298 | 26% | 33,037 26,543 | 24% | 36,258 | |

Operating expenses I 3,868 | 3,156 | 23’T | 10,977 9,023 | 22"% | 12,325 |

Pre-provisioning operating 7,805 profit | 6,142 | 27% | 22,060 17,520 | 26°/» | 23,933 |

Loan losses and provisions 2,043 | 1,248 | 64% | 5,637 3,321 | 70* | 4,631 |

Share of profit of associates 3 | 2 | 50% | 9 5 | 80% | 8 |

Profit before tax 5,765 | 4,896 | 18% | 16,432 14,204 | 16% | 19,310 |

Profit after tax 4,308 | 3,639 | 18% | 12,234 10,627 | 15% | 14,451 |

Profit after tax attributable to- |

|

|

|

| |

Owner's of the Company 4,246 | 3,639 | 17% 12,158 10,627 | 14% | 14,451 | |

Non-controlling interest 62 |

| ' 76 |

|

| |

” Others include other operating income and other income

STANDALONE PERFORMANCE HIGHLIGHTS

Ba|a| Finance Limited — Q3 FY25

Assets under management grew 26% to Rs 293,370 crore as of 31 December 2024 from Rs 232, 040 crore

as of 31 December 2023.

Net interest income increased by 22% in Q3 FY25 to Rs 8,500 crore from Rs 6,973 crore in Q3 FY24.

Pre-provisioning operating profit increased by 26% in Q3 FY25 to Rs 6,986 crore from Rs 5,539 crore in Q3

FY24

Loan losses and provisions for Q3 FY25 was Rs 2,008 crore as against Rs 1,248 crore in Q3 FY24.

< Profit before tax increased by 16% in Q3 FY25 to Rs 4,978 crore from 4,291 crore in Q3 FY24.

Profit after tax increased by 17% in Q3 FY25 to 3,706 crore from 3,177 crore in Q3 FY24.

Gross NPA and Net NPA as of 31 December 2024 stood at 1.41% and 0.61No respectively, as against 1.18% and 0.46*» as of 31 December 2023. The Company has provisioning coverage ratio of 57% on stage 3 assets.

PERFORMANCE HIGHLIGHT OF SUBSIDIARIES

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Bajat Housinq Finance Limited — Q3 FY25

Bajat Housinq Finance Limited — Q3 FY25

As Gets under management grew by 26% to 7 108,314 crore as of 31 December 2024 from 7 85,929 crore

as of 31 December 2023

Net interest income increased by 25% in Q3 FY25 to 806 crore from 645 crore in Q3 FY24.

Net total income increased by 25% in Q3 FY25 to 933 crore from 746 crore in Q3 FY24 Loan losses and provisions in Q3 FY25 was Rs 35 crore as against Rs 1 crore in Q3 FY24.

Profit after tax increased by 25% in Q3 FY25 to 548 crore from 437 crore in Q3 FY24.

Gross NPA and Net NPA as of 31 December 2024 stood at 0.29*â and 0.13% respectively, as against 0.25*S and 0.10% as of 31 December 2023. BHFL has provisioning coverage ratio of 55*' on stage 3 assets.

Capital adequacy ratio (CRAR) (including Tier-II capital) as of 31 December 2024 was 27.86"/

BHFL enjoys the highest credit rating of AAA/Stable for its long-term debt programme from CRISI L and India

Ratings and Al+ for short-term debt pfogramme from CRISIL and India Ratings.

D - Summary of standalone financial results of Bajai Housing Finance Limited

Rs in crore)

Particulars | Q3’25 Q3'24 QoQ | 9M'25 | 9M'24 | 9Mo9M | FY24 | ||

Assets under management | 108,314 85,929 | 26% I 108,314 | 85,929 | 2655 | 91,370 | |||

Assets under finance | 95,570 ' 73,197 | 310/ 95,570 | 73,197 | 31% | 79,301 | |||

Interest income | 2,322 1,846 , 26’% 6,612 | 5,295 | 251Ă | 7,202 | |||

Interest expenses | 1,516 1,201 261Ă 4,428 | 3,413 | 30"% | 4,692 | |||

Net interest income | 806 | 645 25% | 2,184 | 1,882 | 16% | 2,510 | |

Fees and commission income | 49 | 32, 535a i 150 | 95 | 58*S | 138 | ||

Net gain on fair value changes | 41 27 52"/« 137 | 98 | 40% | 133 | |||

Income on de-recognised loans and Sale of services | 23 30 (23*â) 130 | 105 | 24° | 106 | |||

Others” | 14 12 | 17% 38 | 28 | 36*S | 38 | ||

Nettotalincome | 933 746 | 25% 2,639 | 2,208 | 20% | 2,925 | ||

Operating expenses | 185 173 7% 539 | 509 | 6"/ | 703 | |||

Pre-provisioning operating profit | 748 573 31”/o 2,100 | 1,699 | 24% | 2,222 | |||

Loan losses and provisions | 35 1 50 | 26 | 92"% | 61 | |||

Profitbeforetax | 713 572 25% | 2,050 | 1,673 | 23% | 2,161 | |||

Profit after tax | 548 | 437 25% t 1,576 | 1,350 | J7% | I ,731 | ||

“ Others include olher operating income and olher income

Bataj Financial Securities Limited — Q3 FY25

Bajaj Finsec acquired approximately 75,000 customers in Q3 FY25 Overall customer franchise stood at approximately 908, 000 as of 31 December 2024.

Marg in trade financing (MTF) book grew by 70% to ' 5,392 crore as of 31 December 2024 from I 3,167

crore as of 31 December 2023.

Profit before tax increased by 127% in Q3 FY25 to 7 50 crore from 7 22 crore in Q3 FY24

Profit after tax increased by 119% in Q3 FY25 to 7 35 crore from 7 16 crore in Q3 FY24.

E - Summary of results of Ba)ai Financial Securities Limited

| 7 in crore | |||||||

Particulars | Q3’25 | Q3’24 | QoQ | 9M’25 |

| 9M’24 | 9Mo9M | FY24 |

Assets under finance (MTF Book) | 5,392 | 3,167 | 70’/ | 5,392 |

| 3,167 | 70% | 3,817 |

Interest income | 163 | 88 | 85*1 | 453 |

| 199 | 128* | 318 |

Interest expenses | 94 | 57 | 65 | 272 |

| 125 | 118? | 206 |

Net interest income | 69 | 31) | 123% | 181 |

| 74 | 145% | 112 |

Fees and commission income | 33 | 31 | 6’1, | 122 |

| 83 | 47% | 126 |

Net gain on fair value changes | (1) | 11 | (109%) | 18 |

| 28 | (36*) | 36 |

Others* | 9' | 1 | 800”/ | 12 |

| 4 | 200"/ | 6 |

Net total income | 110 | 74 | 49% | 333 |

| 189 | 76% | 280 |

Operating expenses | 60 | 52t | 15*S | 195 |

| 143 | 36?? | 207 |

Pre-provisioning operating profit | 50 | 22 | 127% | 138 |

| 46 | 200% | 73 |

Loan losses and provisions [Q3 FY25 7 (0 04) crore, Q3 FY24 7 0.46 crore] |

|

|

|

1 |

|

1 |

0% |

2 |

Profit before tax | 50 | 22 | 127% | 137 | ! | 45 | 204% | 71 |

Profit after tax | 35 | 16 | 119% | 103 |

| 34 | 203% | 56 |

* Others incur de dividend income other operating income and other income

% Shareholding and

% Shareholding and Particulars

Particulars

BFL BHFL BFinsec Consolidated 2023 Growth

BFL BHFL BFinsec Consolidated 2023 Growth 46,827 t

46,827 t -

- t

t