Diversified Financials: At this juncture, it appears that the risk in FY2027E may be more to growth than asset quality.

FinTech BizNews Service

Mumbai, 25 May 2026: The latest Kotak Institutional Equities report focuses on Diversified Financials;

Encouraging trends

Amid uncertainty due to the West Asia conflict, 4QFY26 was a blockbuster quarter for NBFCs, with better-than-expected asset quality trends and a cautiously optimistic outlook while acknowledging macro challenges. Higher inflation/fuel prices/rates may pose risks to an otherwise strong FY2027E. Despite earnings upgrades following the results, we retain some buffers to estimates, implying upsides in a favorable scenario. At this juncture, it appears that the risk in FY2027E may be more to growth than asset quality.

A superlative quarter

Strong asset quality. 4QFY26 was a strong quarter with improvement in the asset quality performance across most NBFCs under coverage across most buckets. It appears that weakness in the last week of March (due to fuel shortages) had negligible impact on the sector. More importantly, the ailing small ticket MSME loan segment also reflected signs of stabilization. Select NBFCs, viz., Bajaj Finance (3 bps), Chola (9 bps) and Mahindra Finance (16 bps) made extra provisions to buffer for forthcoming macro challenges.

Loan growth continued to accelerate. This was likely buoyed by post-GST cut demand, with disbursements even in some of the sluggish segments of affordable HFCs and small-ticket MSMEs showing signs of turnaround. With macro challenges on the horizon, we model loan growth toward the lower end of management guidance, exceptions include gold loan NBFCs or companies that purchased gold loans (LTF). Current strong trends and ECL buffers suggest that while there may be limited risk/downside shocks to our credit cost estimates, any supply shocks due to higher fuel prices may nudge lenders to go slow and have downside risk to growth.

Mixed margin trends. Continued fall in average cost of funds, amid higher bond yields, aided NIM even as trends in yields have been divergent. Margins of affordable HFCs are close to peak, albeit with recent PLR cuts. Non-interest income growth was strong; a large part of this may be attributed to efforts to improve fees and higher insurance income. While we stare at rate hikes (banks already started to hike MCLR in select buckets), we expect FY2027E to be a tale of two halves. Funding costs have seen a progressive fall in 1QFY26-4QFY26. We expect a higher funding cost base to support yoy margin expansion in 1HFY27, while expecting some compression in 2HFY27 as rates rise. A positive outcome of potential rate hikes is the lower rate wars hereon. Considering the above, we do not build in significant margin compression in FY2027E.

Retain positive, cautiously optimistic stance

We remain assertive about the sector, while remaining cautious of the changing macro—fuel price rise/inflation, slowing economic growth and bond yields. We prefer to stick to high-quality names, reiterating positive calls for Bajaj Finance and Chola. Aditya Birla Capital is our top pick among emerging names. Among smaller (mid-cap) names, Aadhar and Aptus remain favorite picks.

We do not rule out upside risks despite high growth expectations

We have baked in significant buffers in our estimates for NBFCs to account for the macro uncertainties. In a favorable scenario of quick retraction in fuel prices, we find upgrades to our estimates.

4 | Aditya Birla Capital (standalone) reported 27% loan growth in FY2026; the company expects to maintain the momentum, with an increasing share of personal/retail loans expanding RoA by ~20 bps. We are building in 23% loan growth in FY2027E with a stable RoA. In the case of macro adversities being lower-than-expected, the company exceeds our forecasts. It recently announced a proposal to raise capital of Rs40 bn (14% of net worth); according to the company, 87.5% of the same may be deployed in the company’s lending business. As such, higher-than-expected loan growth can provide upsides to our estimates. |

4 | Bajaj Finance remains confident about achieving 22-24% AUM growth in FY2027E and 23-25% AUM growth over the longer term; we bake in a 22% AUM growth in FY2027E at the lower end of the guidance. We bake in a sharp 40 bps NIM compression in FY2027E and a further 20 bps in FY2028E to account for elevated competition. While Bajaj’s management has guided for 25-40 bps improvement in the cost ratio, owing to operating leverage and AI gains, we build in a reduction of just 20 bps per year. On credit costs, the company has guided for 15-30 bps yoy reduction in credit costs (we bake in 20 bps) after building in a buffer of 10 bps in FY2026. |

4 | Chola has guided for 20-23% loan growth for FY2027E versus guidance of 20-25% last year (KIE estimate of 22%). We bake in 10 bps NIM compression for Chola against stable NIM trajectory guidance from management. We also bake in credit costs of 1.5% over FY2027-29E against a long-term average credit cost of 1.25% over FY2017-26 (1.6% in FY2026); management has created extra provisions of 9 bps in FY2026, which provides a buffer. |

Strong growth for diversified players; retail picking up slowly

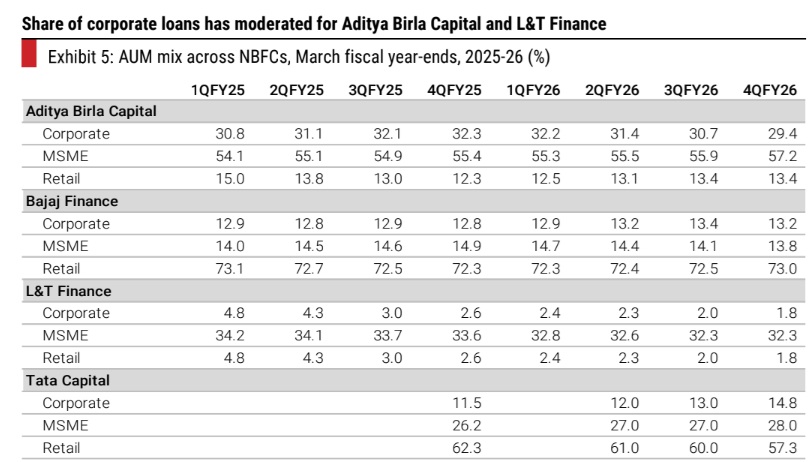

AUM growth remains broadly strong, but with increasing divergence between diversified lenders and monoline players. Diversified lenders such as Aditya Birla Capital, Bajaj Finance, Cholamandalam, L&T Finance and Tata Capital continue to report >20% AUM growth in FY2026, supported by robust disbursements and strong demand across the consumer, SME and vehicle segments.

4 | Retail loans gaining incremental traction; mixed trends in wholesale loans. Growth in wholesale loans was strong in 1HFY26 and FY2024-25, supporting overall AUM growth for players such as Aditya Birla Capital and Tata Capital; retail and unsecured disbursements picked up in 3QFY26 and remained strong in 4QFY26 as well. Notably, corporate loans reported 55% growth for Tata Capital versus 20% growth in retail (ex-TMFL). Aditya Birla Capital (standalone), on the other hand, reported 27% loan growth in FY2025 in corporate loans, which consciously moderated to 15% by FY2026; personal and consumer loans grew 38% in FY2025 from an 11% decline in FY2025. Wholesale loans continued to decline for LTF, down 14% yoy. |

4 | Affordable HFC/MSME loan growth moderates, disbursement picks up. Monoline NBFCs such as MSME-focused lenders and HFCs have reported some moderation in AUM growth due to (1) elevated competitive intensity from banks and large NBFCs and (2) a cautious stance on lower‑ticket borrowers and LAP segments. Disbursement growth for affordable housing players was a tad weak at 3-14% during 2Q-3QFY26, but has picked up to 11-24% yoy in 4QFY26. While 4Q tends to be a seasonally strong quarter, the pick-up in disbursements may indicate stabilization of competitive intensity and asset quality parameters in the segment. We have revised down our loan growth estimates for the next two years by 1-5%, extrapolating recent disbursement trends. |

4 | Gold loan segment witnessed a spike, driven by a sharp rise in gold prices. While gold prices were up 75% yoy in FY2026, Muthoot reported 50% AUM growth compared with 100-150% AUM growth reported by peers such as IIFL and Manappuram Finance. The constraint for Muthoot is its ability to raise borrowings; hence, it has grown at 10-12% qoq in the past five quarters, despite a higher rise in gold prices. The recent rise in gold prices (due to an increase in duties) provides a further tailwind to growth. |

NIM: Mixed trends, may come off moderately in FY2027E

Margins are showing a mixed-to-softening trend across the coverage universe, reflecting the lagged impact of rate cycles and evolving product mix. Large diversified NBFCs such as Aditya Birla Capital (down 17 bps to 5.1% in FY2026), Bajaj Finance (down 23 bps), L&T Finance (down 37 bps) and Tata Capital (down 45 bps) reported NIM compression due to higher funding costs. Affordable housing financiers have fared better (up 8-31 bps yoy) in FY2026, but continue to face structural margin pressure from competitive intensity and transmission of lower rates. However, vehicle lenders such as Cholamandalam and Mahindra Finance buck the trend—have reported margin expansions (up 12-26 bps in FY2026), supported by a lower cost of funds.

Liability side benefits continue in 1HFY27E, on a high base. The benefit of the RBI’s repo rate cut has accrued to NBFCs through the course of the year, leading to a gradual moderation in the cost of borrowings to 6.9-8.6% in 4QFY26 from 6.8-9.2% in 2QFY26 and 7.2-9.4% in 4QFY25. Yields were also down to 8.8-24.3% by 4QFY26 from 9.4-25.5% in 4QFY25 as NBFCs passed on the benefit of the rate cut to borrowers.

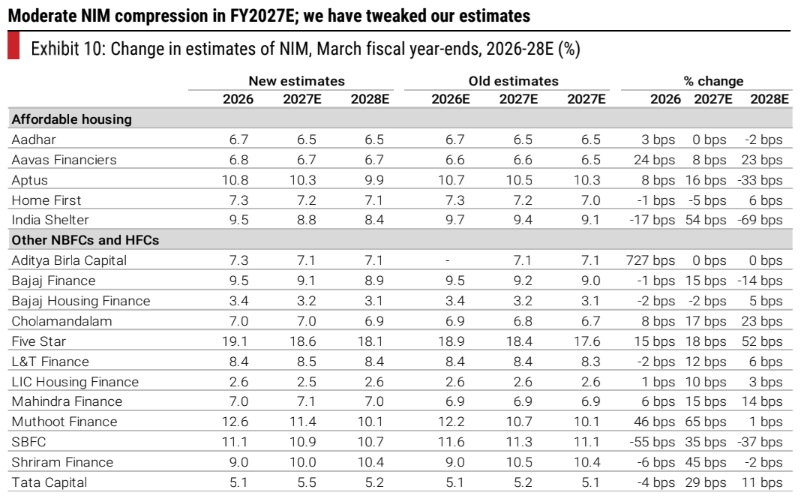

Moderate NIM compression in FY2027E. Overall, sector NIMs will likely moderate in FY2027E, driven by (1) the rise in the cost of borrowings as bond yields harden and (2) elevated competitive intensity exerting pressure on yields. While margins in the first half will likely remain buoyant due to a high base of the cost of borrowings in 1HFY26, the lower base and elevated competition will compress spreads in 2HFY27E. On the positive side, the onset of a rising rate regime and West Asia conflict has significantly reduced the rate wars; as such, the risk to yields is much lower than initially anticipated. Continued rate hikes (our economist pens down a 50 bps policy rate hike) will exert pressure—this will be reflected in FY2028E.

Fee realization improves

The fee-to-AAUM ratio improved for most players to 16-179 bps in 4QFY26 from 12-149 bps in 4QFY25, driving strong growth (27-44% yoy) in fee income during the quarter. The rise in fee income was largely driven by insurance distribution income. Most players have now acquired a corporate agency licenses and are cross-selling standalone insurance products in addition to the credit life policies attached to loans. This has likely driven the strong growth in fee income during 4QFY26 and FY2026. We bake in a largely flat fee-to-AAUM ratio and this remains an upside risk to our estimates for most players.

Assigned loans inched up

Most players have reported a rise in assigned loans during 4QFY26 and FY2026. Under Ind AS, accounting income of assigned loans is recognized upfront, which leads to elevated profitability in the period when the share of assignments rises. HFCs with a high share of non-home loans (such as Aptus and India Shelter) have likely assigned away loans to adhere to the principal business criteria. This trend is likely to be sustained in FY2027E, leading to a rise in the share of assigned loans for most players under coverage.

Collections improved in 3QFY26, accelerated n 4QFY26

While stressed loans shot up for most players in 1HFY26 (up 22-347 bps sequentially) due to extended rains, a GST cut anticipation and more, the rise in collection efficiency drove a significant moderation in 2HFY26 (down 20-190 bps). Despite the moderation, stressed loans remain elevated yoy for (1) affordable housing financiers with high exposure to LAP, (2) vehicle financiers and (3) MSME-focused lenders.

1+ dpd comes down nicely. Some players under coverage reported 1+ dpd ratio (Aavas, Five Star, Home First and SBFC), which is an early indicator of stress. While the ratio has been elevated throughout the year for most players, there was a sequential improvement in 4QFY26 (down 28-63 bps qoq). Despite the seasonal moderation, the 1+ dpd ratio remains elevated yoy (up 20-158 bps) for most lenders, likely due to stress in low-ticket LAP.

Overall stress reduces in almost all segments. Segmental trends in the gross stage-3 ratio of diversified players show significant moderation in stress in unsecured retail (down 20-150 bps yoy in 4QFY26) and a rise in SME stress (up 18-100 bps yoy in 4QFY26). The stress in unsecured retail loans seems to have largely blown over and the elevated delinquencies in vehicle finance have moderated sequentially. Stress in SME will likely to be sustained in 1HFY27E and we will monitor the trends closely in this segment.

Effective expense control

Most NBFCs have demonstrated effective cost control during the year, leading to a 4-56 bps decline in the cost-to-AAUM ratio to 0.4-4.1% by FY2026 from 0.5-4.6% in FY2025. Following Covid, cost ratios were elevated for most NBFCs as they expanded footprint and invested in IT upgradation. The investments have tapered off, likely driving a moderation in cost ratios. The focus is now on increasing productivity and sweating out the investments, driving down cost ratios across players.

Performance highlights of key diversified financial companies: 4QFY26

Aadhar. Aadhar reported a PAT of Rs3.1 bn, up 27% yoy, driven by margin expansion. NII growth was strong at 25% yoy, driven by 20% AUM growth. Disbursement growth picked up to 20% yoy in 4QFY26 (up from 14% in 3QFY26 and 4% in 2QFY26). Calculated spreads were down 16 bps qoq at 6.4%, driven by a 46 bps decline in yields, offset by a 30 bps decline in the cost of borrowing. Credit costs increased 3 bps yoy to 14 bps in 4QFY26, compared with 25 bps in 3QFY26 and 10 bps in 4QFY25. |

Aavas. Aavas reported PAT of Rs1.8 bn, up 18% yoy, driven by margin expansion. Disbursements picked up 36% qoq and 16% yoy to Rs23 bn in 4QFY26, but AUM growth was moderate at 15% yoy. Calculated NIM expanded 12 bps qoq and 40 bps yoy to 7.2%, driven by 31 bps qoq and 63 bps yoy moderation in the cost of borrowings to 7.2%. Credit costs were muted at 12 bps in 4QFY26, driven by a 5 bps qoq moderation in the overall ECL coverage to 70 bps and muted write-offs. |

Aditya Birla Capital. ABCL reported a standalone PAT of Rs7.8 bn, up 19% yoy. The lending business was strong at 27% yoy and 8% qoq, with strong (16% qoq) growth in the unsecured business; on guided lines, the corporate business growth was at the lowest at 3% qoq. Calculated margins remained a tad weak (down 8 bps qoq). Asset quality performance was strong, with just 5% yoy growth in provisions. Opex growth was, however, higher at 34%, exerting pressure on overall earnings growth. |

Aptus. Aptus reported a 26% PAT growth, driven by higher assignment income. NII growth was moderate at 17% yoy, supported by 15% growth in gross loans on the balance sheet; AUMs were up 21% yoy. Reported spread inched up 14 bps qoq and 33 bps yoy. Assignment income was 2.7X yoy, as the company increased the share of direct assignments (5.4% of AUM, up 100 bps qoq and 420 bps yoy). Operating expenses were up 26% yoy. Credit costs, though 2X yoy, were moderate at 0.5% of AUMs. |

Bajaj Finance. Bajaj Finance reported 22% earnings growth in line with AUM growth of 22%. NIM compressed 15 bps yoy and 9 bps qoq to 9.5%, driven by a sharper decline in yields compared with the cost of borrowings. While the opex ratio was nearly stable, credit costs were moderate at 1.6% compared with 2.3% in 4QFY25 and 3.1% in 3QFY26, although morphed by extra provisions and regrouping. |

Bajaj Housing Finance. Bajaj Housing reported 14% earnings growth in 4QFY26, led by 23% AUM growth and 24 bps yoy NIM compression (3.12%) to drive 15% NII growth. Operating expense growth was curtailed at 6% (cost/AUM ratio of 64 bps, down 11 bps yoy), though provisions on a low base were up 87% yoy (credit costs were negligible at 16 bps). |

Cholamandalam. Chola reported 30% earnings growth, 2% above estimates. NII growth was strong at 26% yoy, driven by 21% loan growth and 41 bps yoy NIM expansion, reflecting liability-side tailwinds. Operating expenses were up 27% yoy. Credit costs were elevated at 1.6% in 4QFY26 (1.8% in 3QFY26 and 1.4% in 4QFY25) versus our expectation of 1.3%; this was partially (about 30 bps of credit costs) driven by extra/overlay provisions. |

Five Star. Five Star reported a 4% decline in PAT, while core PBT was up 5% yoy. NII was up 10% on the back of 11% loan growth (disbursements up 17% after 4% growth in 3QFY26, 3% decline in 1HFY26); NIM compressed 65 bps yoy/7 bps qoq, reflecting the rate cut effected by the company last year. Operating expenses saw growth (up 21% yoy) in 4QFY26, pushing opex ratios. Stressed loans were down 42 bps to 14.4%, while credit costs were elevated at 1.8%. |

Home First. Home First reported 43% PAT growth, driven by NIM expansion. NII growth was strong at 37% yoy, driven by 25% AUM growth and 76 bps yoy NIM expansion. Operating expense growth was moderate at 23% yoy. The credit cost (2X yoy) ratio increased 16 bps due to elevated write-offs at 30 bps (14 bps in 3QFY26 and 24 bps in 4QFY25), while overall ECL coverage was at 79 bps (up 3 bps yoy, down 1 bps qoq). |

India Shelter. India Shelter reported 30% yoy PAT growth; NII growth was strong at 34% yoy, driven by 29% yoy AUM growth (includes co-lending AUMs). Recovery from written-off loans supported higher yields for the company. Operating expenses were up 26% yoy, lower than AUM growth of 29% yoy; credit costs moderated to 0.3% from 0.5% in 3QFY26 (down 22 bps) due to lower write-offs. |

L&T Finance. LTF reported 27% earnings on the back of 32% NII growth, driven by 25% AUM growth (20% in 3QFY26). Disbursements were up 62% yoy, driven by strong momentum in consumer loans (up 98% yoy), micro loans (up 41% yoy), LAP (up 67% yoy) and two-wheeler finance (up 58% yoy). |

NIM + fees (calculated) was up 30 bps yoy and down 25 bps qoq. Operating expenses were down 10 bps yoy, up 10 bps qoq. Credit costs were up 10 bps yoy, down 30 bps qoq. |

LICHF. LIC Housing Finance reported 9% earnings growth, with 6% growth in core PBT. NII growth was muted at 3% yoy, driven by 4% loan growth. Disbursement growth was at 10% overall and 8% for individual home loans. NIM was down 6 bps yoy at 2.8%. Operating expenses were down 12% yoy, driving a 9 bps yoy moderation in the cost-to-AAUM ratio to 51 bps. The credit cost (down 32% yoy) ratio was low at 9 bps, driven by a 20 bps qoq decline in overall ECL coverage to 1.4%. |

Mahindra Finance. Mahindra Finance reported 39% growth in core earnings. AUM was up 12% yoy on the back of 11% growth in disbursements. Calculated NIM expanded 70 bps yoy to 7.3%, reflecting liability-side tailwinds; fees were up 44%, reflecting focus on distribution/insurance income. Opex growth was curtailed at 8% yoy. An increase in provisions by 23% led to 55% growth in earnings, 8% below estimates. |

Muthoot Finance. Muthoot Finance reported 105% earnings growth, driven by 50% yoy/10% qoq loan growth and 200 bps NIM expansion, leading to 80% NII growth. Operating expense growth was muted at 7% yoy, leading to a sharp 96 bps yoy decline in the cost-to-AAUM ratio to 2.4%. Credit costs were elevated at 0.6%, likely due to the shift in NPA classification norms. |

SBFC. SBFC reported 29% PAT growth with 30% NII/29% AUM growth in 4QFY26. Reported NIM compressed 10 bps qoq/expanded 15 bps yoy to 10.2%. Operating expense growth was muted at 9% yoy, leading to a sharp 69 bps yoy moderation in the cost-to-AAUM ratio to 3.9%. Credit costs were elevated at 1.4% (1% in 4QFY25 and 1.3% in 3QFY26), driven by write-offs of 0.8% and stable overall ECL coverage of 1.8%. |

Shriram Finance. Shriram Finance reported PAT of Rs30 bn in 4QFY26, up 41% yoy, driven by a decline in the cost of borrowings and moderation in opex. NII growth was strong at 21% yoy, driven by 15% AUM growth and 47 bps yoy NIM expansion. Operating expenses were down 2% yoy, driven by (1) a moderation in employee count, down 5% yoy and (2) the deferral of DSA payout on 2W loans (Rs500 mn). Credit costs were moderate at 1.9% (1.8% in 3QFY26 and 2.4% in 4QFY25). |

Tata Capital. Tata Capital’s PAT was up 47% yoy, reflecting sustained operating momentum, lower credit costs and operating leverage. NII was up 19% yoy due to 20% growth in net AUMs. Calculated NIM was 5.2%, flat yoy, supported by capital infusion; reported spreads were down 35 bps yoy to 4.3%, likely reflecting faster growth in corporate loans (up 56% yoy, 14% of AUMs) and SME (up 35% yoy, 27% of AUMs). Credit costs were down 60 bps yoy to 88 bps (on high base of provisions in CV book). |