Indian Financial Services Sector must grow 20X with banking playing critical role for Viksit Bharat Mission: FICCI-IBA-BCG Report: While India Stack has enabled excellence in payments, banks still need to monetize the digital opportunity across other dimensions like product fulfillment journeys and money insights

FICCI and IBA in association with BCG released a report titled ‘Banking for a Viksit Bharat’ at FIBAC 2024

FinTech BizNews Service

MUMBAI, 6 September 2024: FICCI and IBA in association with BCG has released a report titled ‘Banking for a Viksit Bharat’ at FIBAC 2024. As per the report, India's ambition to achieve a $30 trillion GDP by 2047 will require a 20 times growth in the financial services sector, with banks playing a pivotal role. India, being a predominantly bank-led economy, will require the banking sector to play an anchor role while the other financial asset classes continue to grow much faster. This will require $4 Tn of capital base in banks, 1/3rd of which will have to be fresh capital deployment. India's banking system is in a strong position today – characterized by high profitability, robust capital adequacy, and low levels of non-performing assets (NPAs). This provides an ideal launchpad for the Viksit Bharat mission.

Ms Jyoti Vij, Director General at FICCI, and Co-author of the report said, “India’s Digital Public Infrastructure has laid the foundation for a strong and resilient financial infrastructure and accelerated the pace of digitization. It is now about taking capabilities to the next level and building for the next two decades - Resilience, climate and cyber security needs to be strengthened, with centralized, real-time network and specialized talent. The banking sector’s success is instrumental in making India a developed nation.”

Mr MV Rao, Chairman at Indian Banks’ Association, and Co-author of the report said, “One of the primary objectives of the banking industry is to ensure financial inclusion, creating opportunities for every individual to grow and contribute to the nation’s progress. To fuel inclusion and credit growth, we must continue to innovate and reimagine our deposit strategies, aligning them more closely with the evolving needs and preferences of our customers. This growth will be aided by the full potential of our workforce which must be harnessed using digitization and emerging technologies like GenAI.”

Mr Ruchin Goyal, Managing Director and Senior Partner at BCG, and Co-author of the report said, "The journey towards a $30 trillion economy by 2047 is an ambitious yet achievable goal for India, demanding a transformation in the financial services sector, with banks at the forefront. India's banking system is in a strong position today acting as an ideal launchpad for the Viksit Bharat mission. It will have to build for the next 2 decades through structural shifts – growing deposits, enhancing asset quality, and improving productivity, while advancing digital capabilities and future competencies.”

The report highlights five key structural themes that banks need to work on for continued success of Indian banking sector.

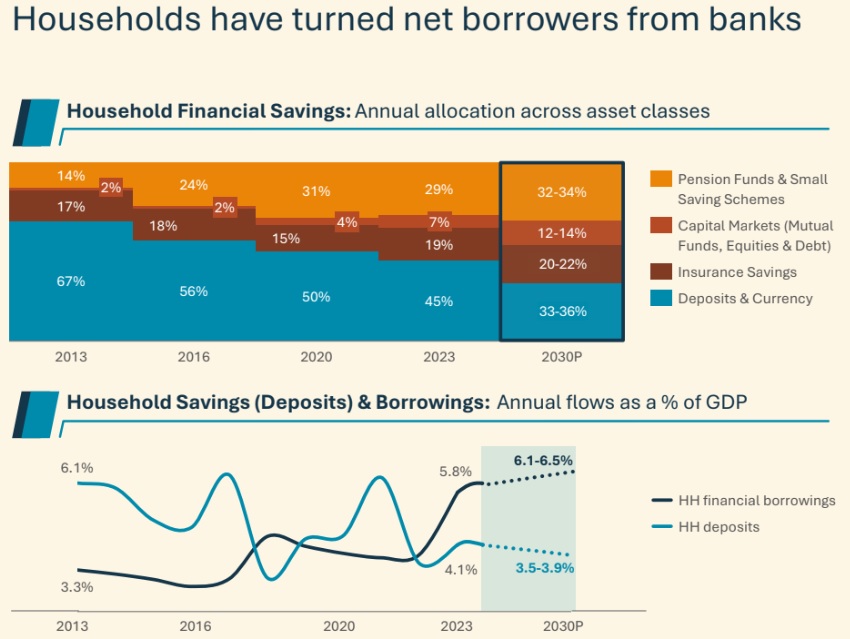

A) Future of Household savings:

Households are increasingly shifting from physical to financial assets, and from informal to formal borrowing channels. Bank deposits are shifting to pension savings and capital market investments, while retail lending expands. Despite this, financial assets and borrowings remain under-penetrated, offering significant growth potential. Banks must innovate deposit products, enhance customer awareness, and adopt new operating models to sustain growth. Structural support is needed to create new deposit pools for targeted lending, as banks continue to play a key role in funding large-scale projects and sectors.

B) Addressing challenges with asset quality & pockets of leverage:

Retail lending has driven financial inclusion and profitability for the banking industry. The shape of this growth is very different though. Unsecured lending has grown much faster. The unsecured to secured loan mix is 30:70 in India (vs. 10:90 for many large economies). India has a large adult population outside the formal workforce (~90%), and hence largely outside the ambit of formal financing channels. India has quickly gone from being a data-poor to a data-rich country. Lenders will have to re-imagine the operating model and underwriting capabilities to serve this segment. India will need to chart its own course on driving retail and MSME lending penetration.

C) Banks need to take a bold vision on productivity:

India Stack has revolutionized the financial infrastructure, driving digitization in payments and product sales. However, rising costs, driven by increased technology spending, outpace income growth. Despite high tech spending, banks globally are not seen as innovative, and Indian banks are still under indexed in IT investments. Banks will need to boldly reimagine their operating model and break the 'sticky' legacy cost structure.

D) Banks to continue investing to drive digital funnel growth:

Leading Indian banks rank among the top globally in digital maturity, with BCG's proprietary benchmarking tool showing that both private and public sector banks score higher than global peers across various parameters related to customer experience. Many banks need to continue investing to bridge the gap. While India Stack has enabled excellence in payments, banks still need to monetize the digital opportunity across other dimensions like product fulfillment journeys and money insights.

E) Banks to focus on building future capabilities:

The Indian banking system has made significant strides in building future-ready competencies but must embrace the next wave of opportunities. Resilience must extend beyond technology to encompass entire business processes. Banks face a "GenAI paradox," struggling to scale initiatives beyond pilots. This will require mission-mode COEs to address key capability challenges. Climate risk presents both threats and a $2.5 trillion financing opportunity, demanding a shift in operating models. Additionally, India’s banks must tackle increasing cyber risks, necessitating a centralized, real-time network and specialized talent to mitigate threats.

While India's banking sector has made significant strides, achieving the Viksit Bharat mission will require sustained momentum. The banking sector’s success is instrumental in making India a developed nation.

A concerted effort of industry participants, government and regulator will be critical to facilitate this – key actions include: