Equirus Wealth Report Based on Five-Year Study: 75–90% of women investors now hold through market corrections rather than exiting in panic

FinTech BizNews Service

Mumbai, March 5, 2026: Equirus Wealth, one of India's fastest-growing wealth management firms managing over Rs35,000 crore in assets among the country's top 10 non-bank wealth managers, has released a landmark report titled “Expanding Horizons: Changing Wealth Management Behaviours of Indian Women - Qualitative Analysis of Investor Evolution Across Age and Affluence.”

Beyond the Stereotype: A Multi-Dimensional Evolution

The report, draws on insights from interactions with approx. 55,000 women investors and more

than 100 relationship managers over a five-year period. It examines how investors across Mass

Affluent, HNI and UHNI| Family Office segments are evolving their approach to portfolio

construction, risk perception, advisor relationships and legacy planning.

It covers three age cohorts: Young (25–35), Mid-Career (36–50), and Senior (51+).

The study reveals women investors are increasingly moving away from episodic product purchases

such as fixed deposits, gold and property towards diversified, allocation-driven portfolios anchored

around long-term financial goals.

According to the report ,Artificial Intelligence may dominate global investment conversations, but

Indian women investors are adopting it cautiously — using it primarily as research and learning tool

rather than for autonomous investment decisions.

The findings also point to a structural shift in behaviour — from product-led investing to disciplined,

allocation-driven portfolio frameworks. What it reveals is not incremental progress—it is a structural

reinvention of how women engage with capital, mapping shifts in portfolio construction, risk

perception, macro awareness, advisor relationships, and legacy planning.

Commenting on the findings, Ankur Punj MD- Business Head, Equirus Wealth said: “Indian women

investors are becoming more informed, confident and strategic in shaping their financial futures.

Over the past five years we have seen a clear shift from buying individual financial products to

building structured portfolios anchored around asset allocation and long-term goals. Technology,

including AI, is beginning to play a role in the learning and research process — but disciplined

frameworks and human judgement continue to guide investment decisions.”

Key Findings from the Five-Year Study:

The Allocation Revolution:

Fixed Deposits have seen their share in portfolios drop from 45% to 20% over five years, while Equity

Mutual Funds have surged from 10% to 32%. Alternatives (PMS/AIF) have grown from a negligible

3% to 7%.

Five years ago, the dominant pattern among Indian women investors was familiar: fixed deposits,

gold, and property—the classic ‘safety-first’ portfolio. Today, the same cohort has migrated toward

allocation-led, goal-mapped portfolios that include equity mutual funds, structured debt products,

AIFs, PMS, and in some cases, global equities and private markets.

75–90% Hold through market corrections—‘wait and review’ dominates

55% Add capital selectively in market dips—conviction-led

↑ 80% Macro influence rated high (4–5/5) today vs.1–2/5 five years ago

75–100% Reference advisor but nowdemand explanation—not just trust

AI Is Emerging as a Learning Layer — Not a Decision Maker

While AI tools are entering the investment ecosystem, adoption among women investors remains

measured.

The study finds that 35–50% of women investors either do not use AI tools or use them selectively,

primarily for learning, monitoring and research insights. Importantly, final portfolio decisions

continue to rely on human judgement and advisor guidance rather than automated

recommendations.

This suggests that AI is emerging as an information and analytics layer within the investment process

rather than a substitute for human decision-making.

The Bucket Thinking Revolution:

The Bucket Thinking Revolution: Investors are increasingly adopting “bucket thinking” — organising

portfolios around life goals such as safety, growth, liquidity and legacy rather than individual

products — shifting the focus from “Which product should I buy?” to “What role should this asset

play in my portfolio?”, with portfolio discipline increasingly guided by allocation frameworks and

rules rather than market reactions

Stronger Behavioural Discipline During Market Cycles

Women investors are showing increasing maturity during market cycles.

Today, 75–90% of investors hold or review their investments during market corrections rather than

exiting in panic. At the same time, around 55% selectively add capital during market dips, reflecting

growing conviction and a longer-term approach to investing.

The Death of Product Push

The study finds a definitive shift toward "allocation-led" thinking. Investors are now segmenting

portfolios into "buckets" for safety, growth, goals, and legacy, rather than simply collecting financial

products.

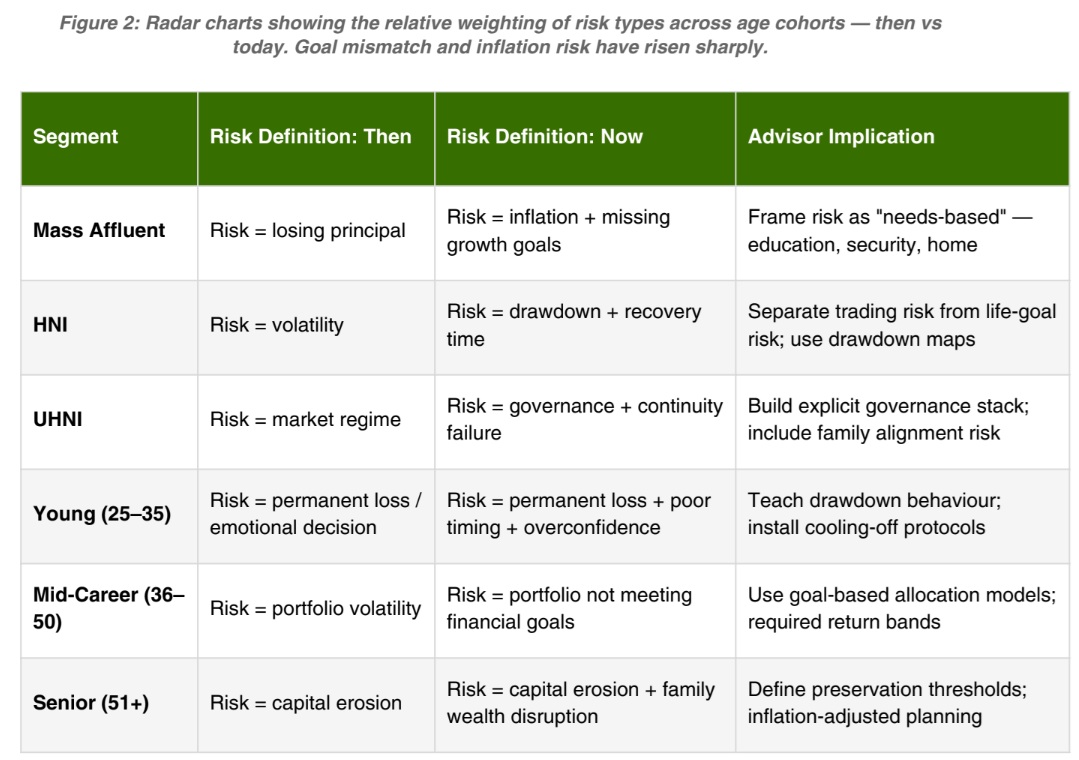

Risk Is Being Reimagined—Not Just Reduced

Women investors are also developing a more nuanced understanding of investment risk.

Five years ago, risk was largely interpreted as loss of principal. Today it increasingly includes inflation

erosion, failure to meet financial goals, portfolio drawdowns and recovery time, as well as

governance risks within family wealth structures.

This shift reflects growing financial awareness and investment sophistication across investor

segments.

Evolution of the Advisor Relationship

The study highlights a transformation in the advisor-client relationship.

Women investors increasingly evaluate advisors based on transparency, proactive strategy, financial

education and governance support, rather than simply product access. As a result, the advisor

relationship is evolving from product distribution toward strategic partnership in portfolio

construction and wealth governance.

Legacy Is No Longer an Afterthought

Intergenerational wealth transfer is emerging as a key priority with 75–90% of respondents actively

discussing legacy planning to ensure next-gen beneficiaries have the right behavioural guardrails.

Inheritance is increasingly viewed not just as a transfer of capital but as a transfer of financial

discipline and investment frameworks, ensuring that future generations are equipped to manage

wealth responsibly. Succession and intergenerational wealth transfer have moved to the forefront,

particularly among HNI and UHNI women investors who are taking active roles in family governance

and estate planning.

In conclusion What the Industry Must Do Now.

The report identifies three non-negotiable imperatives for wealth managers serving this evolving

cohort:

Build a portfolio “operating system”, not a product pitch. Start with a clear portfolio map

that defines the role of each asset bucket, expected drawdown ranges and a disciplined

review cadence

Shift the conversation from return maximisation to goal protection. Many women

investors increasingly define risk as goal failure, inflation erosion or poor decisions during

market stress

Translate macro events into clear portfolio actions. Investors are looking for simple

guidance — what has changed, what has not, and whether the right response is to

rebalance, hold or add

Bring stronger governance frameworks into wealth management. Particularly for HNI and

UHNI families, this includes clearer decision rights, Investment Policy Statements (IPS),

committee processes and reporting that separates signal from market noise

Build investor confidence through education and structure. Regular reviews, transparent

communication and small investment milestones help investors participate more actively in

portfolio decisions

Use digital and AI tools as an explainability layer. Technology is welcomed when it

improves understanding and monitoring, but investors continue to rely on human

judgement for final decisions