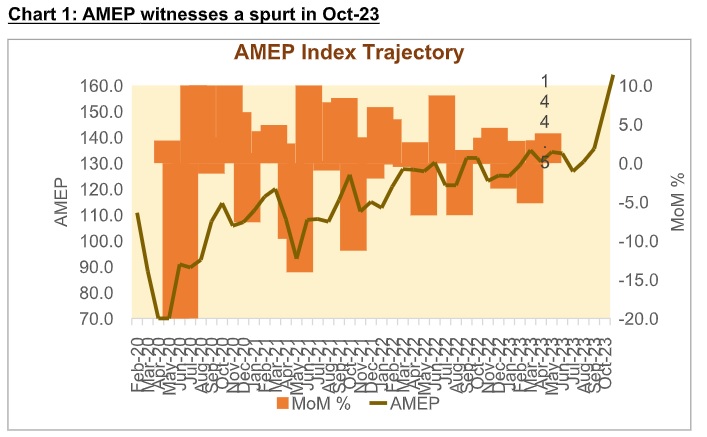

Festival fever drives AMEP to a peak in Oct-23

FinTech BizNews Service

Mumbai, November 22, 2023: Acuité Macroeconomic Performance index (AMEP index) has touched an all-time high in Oct-23 since the series began in Aug 2019, following a strong performance in the second quarter of the current fiscal. This has been primarily driven by heightened economic activity and a surge in consumer demand that is in action during the festival season of Oct-Nov. The index has seen a rise of 6.6% on a sequential basis compared to that in Sep-23 but encouragingly, it has also grown strongly by 9.5% YoY, reflecting the continuation of a strong momentum in the economy that remains supported by increased public expenditure in infrastructure development and steady urban demand particularly for services apart from the consumption boost provided by festivities and also special events like the ICC World Cup 2023. Among the sixteen high frequency indicators in the index, almost all of them i.e. fifteen indicators have notched up a positive growth on an annualised basis with the sole exception of only tractor sales.

Given the step up in the spending in the Indian infrastructure sector, there has been a strong growth in steel production in the current year at 13.3% YoY in H1FY24. That trend has continued in Oct-23 with output growth at 10.3% YoY and 0.6% MoM.

One of the indicators reflecting a rise in consumption demand during the festive season is automotive sales (passenger vehicles, two and three wheelers) volumes which increased by 17.1% YoY and 6.0% MoM. Apart from the push from festive demand, launch of new vehicle models particularly in the SUV category, improved availability of semi-conductor chips and the ongoing state elections have also given an impetus to auto sales. SIAM (Society for Indian Automobile Manufacturers) has reported that the volumes in Oct-23 were the highest ever for the PV and 3W category. While the growth in 2W sales was also robust at 20.1%YoY, the sustainability of such growth will need to be seen given the lack of consistency in rural demand.

Rail traffic has witnessed a significant traction in the previous month, reflecting sustained industrial activity and a spurt in travel during the festival period; both rail freight and rail passenger traffic saw a healthy annualised growth of 8.5% along with strong sequential pickup of 4.4% MoM and 5.1% MoM. Domestic coal production during the month of Oct-23, reached 78.6 mn tonnes (MT), surpassing the figures of 66.3 MT of the corresponding month last year, registering a significant growth of 18.6%; higher mining activity has also therefore translated into increased freight movement.

Another metric that has seen a robust growth in the current year is the demand and consumption of power. In the first half of the fiscal, electricity output rose by 4.8%. The level of power generation increased by 22.2%YoY and 2.5%MoM in Oct-23 partly due to warmer conditions during the month and also partly due to the low base.

Retail fuel i.e., petrol and diesel consumption have also recorded a strong trajectory with 4.8%YoY and 9.3%YoY growth respectively, given the rise in mobility during the festive months. Further, the strong sequential growth in diesel consumption at 17.6% also indicates higher usage by the agricultural sector amidst lower rainfall.

Credit growth (non-food) continues to stand at 19.8% YoY (including the impact of HDFC merger). While the credit growth is gradually getting broad-based, the demand remains high from the services sector, particularly non-banking finance companies (NBFCs) that borrow for on-lending purposes, and retail loans for non-housing purposes. The latest clampdown on retail unsecured loans may slow down the bank credit growth to some extent. Expectedly, the sharp rise in festival induced consumer purchases has led to robust growth in GST collections at 13.4% with E-way bills generation rising more sharply at 30.5%YoY, partly also due to increased compliance with GST rules.

One single indicator that exhibited an annualised contraction was tractor sales; volumes dropped by 4.3%YoY while on a sequential basis, it recovered by 22%. While monthly exports of tractors was the lowest since Jun-20, the rainfall deficiency in the current year and the risks of El Nino may be a factor in tractor demand slowdown. Although the trade deficit figure has of late become a point of concern, both export and import increased by 6.3% and 12.4% YoY respectively in Oct-23. Imports have been driven higher by not only higher value of oil imports but also by the higher gold imports which are linked to the festive and the upcoming marriage season.

While employment growth is currently a structural problem, the all India Employment Rate increased marginally by 3.5%YoY but dropped by 1.3%MoM. As per CMIE, the unemployment rate however, rose to a two-year high of 10.05% in Oct-23. Notwithstanding the fact that most of the demand indicators in October remained strong, India Manufacturing Purchasing Managers’ Index (PMI) declined to an 8-month low in Oct-23 as it dropped significantly to 55.5 from 57.5 in Sep-23. PMI Services also declined to 58.4 from 61.0 in the month before. While the elevated PMI levels still indicate a healthy momentum in economic activities, their trajectories reflect a moderation in growth going forward.

Says Suman Chowdhury, Chief Economist & Head-Research “While the growth print in Q1FY24 was high at 7.8% YoY and is estimated to be 6.7% YoY in the second quarter, the data for which is to be released shortly, there are signs of a moderation in the growth momentum in the second half of the fiscal; we expect 5.0%-5.5% growth in H2FY24 and hold on to our base forecast of 6.0% for FY24. While economic activity in the core sector has continued to be propelled by public investments in the infrastructure sector, persistent headwinds on the export front, higher interest rates along with a tighter funding environment for consumer loans and weaker agricultural output due to the El Nino phenomenon can pose downside risks to the growth trajectory.”

(Disclaimer: Acuité has taken due care and caution for writing this release. Information has been obtained by Acuité from sources which it considers reliable. However, Acuité does not guarantee the accuracy, adequacy or completeness of information on which this release is based. Acuité is not responsible for any errors or omissions or for the results obtained from the use of this release. Acuité has no liability whatsoever to the users / distributors of this release.)