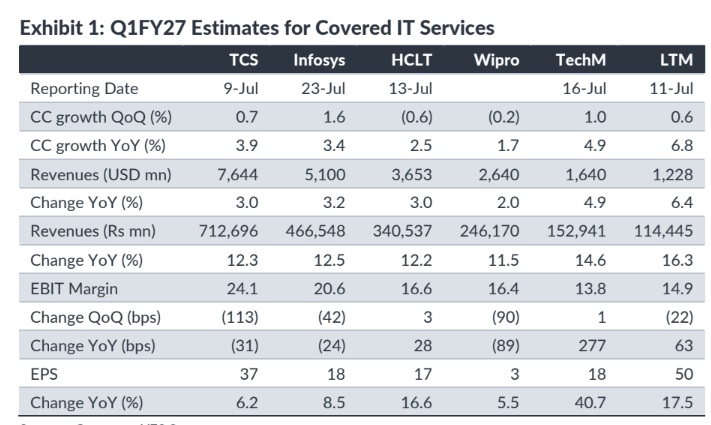

BFSI is expected to remain the most resilient vertical across the IT sector.

FinTech BizNews Service

Mumbai, July 9, 2026: YES SECURITIES has come out with Q1 FY27 Preview report on the Information Technology sector. This provides the brokerage's outlook on the IT services sector ahead of the Q1 FY27 earnings season.

Demand remains soft; discretionary recovery remains elusive; cost takeout continues to dominate

The demand environment remains soft, with macro uncertainty and AI-led ambiguity

continuing to weigh on decision-making cycles. We expect CC QoQ growth to range

from a decline of 0.6% for HCL Tech to a peak of 1.6% for Infosys, with TechM (+1.0%)

and LTM (+0.6%) tracking in between and Wipro extending its underperformance at -

0.2%. Discretionary spending remains largely deferred, and tech budgets are broadly

unchanged even as decision cycles stay elongated. Deal activity remains anchored in

cost takeouts, AI-led productivity engagements, and vendor consolidation. Margins are

expected to remain mixed, with TCS and Wipro facing the sharpest compression from

wage hikes and pricing pressure, while HCL Tech, TechM and LTM supported by

ongoing cost optimization initiatives. BFSI continues to be the most resilient vertical.

TCS: 0.7% CC QoQ growth led by BFSI and life science. Margins to decline to

24.1% due to annual wage hikes and continued investments in AI capabilities.

Infosys: 1.6% CC QoQ revenue growth led by acquisitions and gradual recovery in

BFSI and EURS. FY27 margins are expected to be in the midpoint of the guided

range.

HCLT: -0.6% CC QoQ growth due to client specific issues in telecom and

manufacturing verticals. Margins to slightly improve sequentially to 16.6%.

Wipro: -0.2% CC QoQ growth due to delayed revenue conversions. Margins to

decline to 16.4%, due to full quarter impact of wage hikes and continued

investments in AI-native platforms.

TechM: 1.0% CC QoQ growth led by telecom deal ramp ups. Margins to remain

stable supported by Project Fortius.

LTM: 0.6% CC QoQ growth supported by continued ramp-up in life science and

consumer segments. Margins are expected to decline to ~14.9% due to annual

wage hikes.

Revisiting Valuations: We lower our target multiples by ~20% to factor in subdued

demand, pricing pressure and AI-led revenue deflation. However, with valuations

now well below historical averages and much of the near-term uncertainty priced

in, we remain constructive on the sector, with Tech Mahindra continuing to be our

preferred pick.

Revisiting Valuations

Following the sharp correction in IT stocks, we revisit our valuation framework by incorporating

a more conservative DCF approach, factoring in subdued demand, delayed discretionary

recovery, pricing pressure and AI-led revenue deflation. We continue to assume a 5% terminal

growth rate for most companies (3% real growth and ~2% currency tailwind), while adopting a

lower 3% terminal growth rate for Wipro, reflecting its persistent execution challenges and

weaker growth outlook.

The DCF exercise implies forward multiples that are meaningfully below historical averages,

highlighting market concerns around a structurally lower growth trajectory and increasing

productivity-led pricing resets. Accordingly, we recalibrate our valuation framework by blending

DCF-implied multiples with historical trading averages, resulting in a revised multiple band of

~14.5x-24x, implying an average multiple cut of nearly 20% versus our previous assumptions.

Despite the de-rating, we refrain from an aggressive cut in multiples as current valuations already

discount a large part of the near-term uncertainties surrounding AI, pricing pressure and a slower

discretionary recovery. Moreover, Indian large-cap IT companies continue to enjoy structural

advantages in terms of strong balance sheets, resilient deal pipelines and emerging AI

monetization opportunities.

Tech Mahindra remains our top pick, supported by improving execution, a visible margin

turnaround and better growth prospects under the new management. Conversely, while Wipro

screens inexpensive on DCF, we remain cautious given its inconsistent execution and delayed

conversion of deal wins into revenues, limiting the scope for a meaningful re-rating despite

attractive valuations.

Overall, we believe the recent correction has significantly improved the sector's risk-reward

profile, although near-term performance is likely to remain constrained by demand uncertainty

and a gradual recovery in discretionary spending.

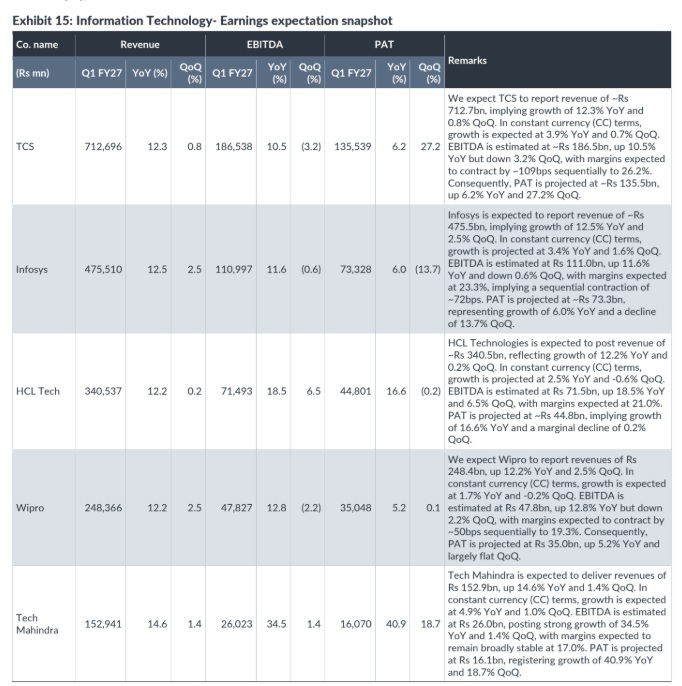

LTM

We expect LTM Ltd to report revenues of Rs

114.4bn, up 16.3% YoY and 1.4% QoQ. In

constant currency (CC) terms, growth is projected

at 6.8% YoY and 0.6% QoQ. EBITDA is estimated

at Rs 19.9bn, up 20.9% YoY and 1.1% QoQ, with

margins expected to moderate to 17.4%. PAT is

projected at Rs 14.8bn, representing growth of

18.0% YoY and 6.3% QoQ.