Unsecured retail advances (incl. retail microcredit) as a % of net advances stood at 10.5% as at December 31, 2024.

FinTech BizNews Service

Mumbai, 18th January, 2025: The Board of Directors of Kotak Mahindra Bank (“the Bank”) approved the unaudited standalone and consolidated results for the quarter ended December 31, 2024, at the Board meeting held in Mumbai, today.

Consolidated results at a glance

Consolidated PAT for Q3FY25 increased to Rs 4,701 crore from Rs 4,265 crore in Q3FY24, up 10% YoY and for 9MFY25 (before KGI divestment) increased to Rs 14,180 crore from Rs 12,876 crore in 9MFY24, up 10% YoY.

PAT of Bank and key subsidiaries given below:

PAT (Rs crore) | Q3FY25 | Q3FY24 | 9MFY25 | 9MFY24 |

Kotak Mahindra Bank | 3,305 | 3,005 | 10,168 | 9,648 |

Kotak Securities | 448 | 306 | 1,293 | 849 |

Kotak Asset Management & Trustee Company | 240 | 146 | 612 | 375 |

Kotak Mahindra Prime | 218 | 239 | 718 | 666 |

Kotak Mahindra Life Insurance | 164 | 140 | 697 | 579 |

Kotak Mahindra Investments | 107 | 157 | 386 | 386 |

Kotak Mahindra Capital Company | 94 | 35 | 265 | 117 |

BSS Microfinance | (50) | 104 | 17 | 307 |

At the consolidated level, Return on Assets (ROA) for Q3FY25 (annualized) was 2.30% (2.46% for Q3FY24). Return on Equity (ROE) for Q3FY25 (annualized) was 12.43% (13.83% for Q3FY24).

Consolidated Capital Adequacy Ratio as per Basel III as at December 31, 2024 was 23.4% and CET I ratio was 22.5% (including unaudited profits).

As at December 31, 2024, Average Liquidity Coverage Ratio stood at 132%.

Consolidated net-worth as at December 31, 2024 was Rs 152,878 crore (including increase in reserves due to RBI’s Master Direction on Bank’s investment valuation of Rs 5,654 crore and gain on KGI divestment of Rs 2,730 crore). The Book Value per Share at December 31, 2024 was Rs 769 (Rs 627 at December 31, 2023).

Consolidated Customer Assets which comprise Advances (incl. IBPC & BRDS) and Credit Substitutes grew to Rs 519,126 crore as at December 31, 2024 from Rs 451,524 crore as at December 31, 2023, up 15% YoY.

Total Assets Under Management as at December 31, 2024 were Rs 686,197 crore up 29% YoY over Rs 533,365 crore as at December 31, 2023. The Domestic MF Equity AUM increased by 39% YoY to Rs 319,161 crore as at December 31, 2024.

Kotak Mahindra Bank standalone results

The Bank’s PAT for Q3FY25 increased to Rs 3,305 crore from Rs 3,005 crore in Q3FY24, up 10% YoY and PAT for 9MFY25 increased to Rs 10,168 crore from Rs 9,648 crore in 9MFY24, up 5% YoY.

Net Interest Income (NII) for Q3FY25 increased to Rs 7,196 crore, from Rs 6,554 crore in Q3FY24, up 10% YoY and for 9MFY25 increased to Rs 21,058 crore, from Rs 19,084 crore in 9MFY24, up 10% YoY.

Net Interest Margin (NIM) was 4.93% for Q3FY25.

Fees and services for Q3FY25 increased to Rs 2,362 crore from Rs 2,144 crore in Q3FY24, up 10% YoY and for 9MFY25 increased to Rs 6,915 crore from Rs 5,998 crore in 9MFY24, up 15% YoY.

Cost to income ratio was 47.24% for Q3FY25.

Operating profit for Q3FY25 increased to Rs 5,181 crore from Rs 4,566 crore in Q3FY24, up 13% YoY and for 9MFY25 increased to Rs 15,534 crore from Rs 14,126 crore, up 10% YoY.

Customers as on December 31, 2024 were 5.2 cr (4.8 cr as on December 31, 2023).

Customer Assets, which comprises Advances (incl. IBPC & BRDS) and Credit Substitutes, increased by 15% YoY to

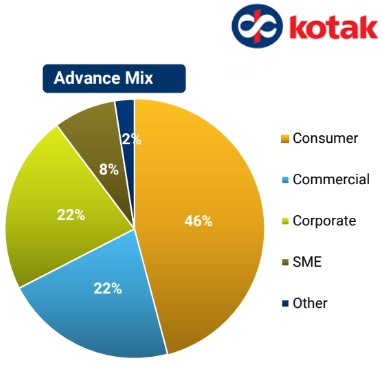

Rs 459,436 crore as at December 31, 2024 from Rs 400,759 crore as at December 31, 2023. Advances (incl. IBPC & BRDS) increased 16% YoY to Rs 433,386 crore as at December 31, 2024 from Rs 372,464 crore as at December 31, 2023.

Unsecured retail advances (incl. retail microcredit) as a % of net advances stood at 10.5% as at December 31, 2024.

Average Total Deposits grew to Rs 458,614 crore for Q3FY25 compared to Rs 398,908 crore for Q3FY24 up 15% YoY. Average Current Deposits grew to Rs 66,589 crore for Q3FY25 compared to Rs 59,337 crore for Q3FY24 up 12% YoY. Average Savings Deposits grew to Rs 124,282 crore for Q3FY25 compared to Rs 123,227 crore for Q3FY24 up 1% YoY. Average Term Deposits grew to Rs 267,743 crore for Q3FY25 compared to Rs 216,344 crore for Q3FY24 up 24% YoY.

CASA ratio as at December 31, 2024 stood at 42.3%.

Credit to Deposit ratio as at December 31, 2024 stood at 87.4%. TD sweep balance grew 31% YoY to Rs 54,797 crore.

As at December 31, 2024, GNPA was 1.50% & NNPA was 0.41% (GNPA was 1.73% & NNPA was 0.34% at December 31, 2023). As at December 31, 2024, Provision Coverage Ratio stood at 73%.

Capital Adequacy Ratio of the Bank, as per Basel III, as at December 31, 2024 was 22.8% and CET1 ratio of 21.7% (including unaudited profits).

Standalone Return on Assets (ROA) for Q3FY25 (annualized) was 2.10% (2.20% for Q3FY24).