MOPW: Silver has provided returns of the CAGR of 7.6% from 1990 to 31st October 2024, Indian Equities have recorded CAGR of 14.0% during the same period.

FinTech BizNews Service

November 25 November 2024: According to Alpha Strategist Report from Motilal Oswal Private Wealth (MOPW), standard deviation on monthly returns and maximum drawdowns for the period between 1990 to 31st October 2024, silver has exhibited volatility similar to Indian equities.

The standard deviation for Silver is 26.6% which is similar to Indian equities at 26.8%. The maximum drawdown of silver is at -54% which is close the maximum drawdown of -55.1% in Indian equities.

Silver has provided returns of the CAGR of 7.6% from 1990 to 31st October 2024, Indian Equities have recorded CAGR of 14.0% during the same period.

Compared to Silver, Gold has provided a meaningful CAGR of 10.6% and scores better on account of recorded standard deviation of 14.7% and maximum drawdown of -25.1%.

Hence, Gold can have a strategic allocation in portfolios, while Silver should be consider only for tactical allocation.

Asset Class | Equity (India) | Gold | Silver |

CAGR from 1990 to 2024* | 14.0% | 10.6% | 7.6% |

Standard Deviation | 26.8% | 14.7% | 26.6% |

Maximum Drawdown | -55.1% | -25.1% | -54.0% |

Maximum Returns -3Y | 59.6% | 32.2% | 26.3% |

Minimum Returns -3Y | -15.6% | -7.3% | -18.4% |

Average Returns - 3Y | 12.9% | 10.3% | 11.7% |

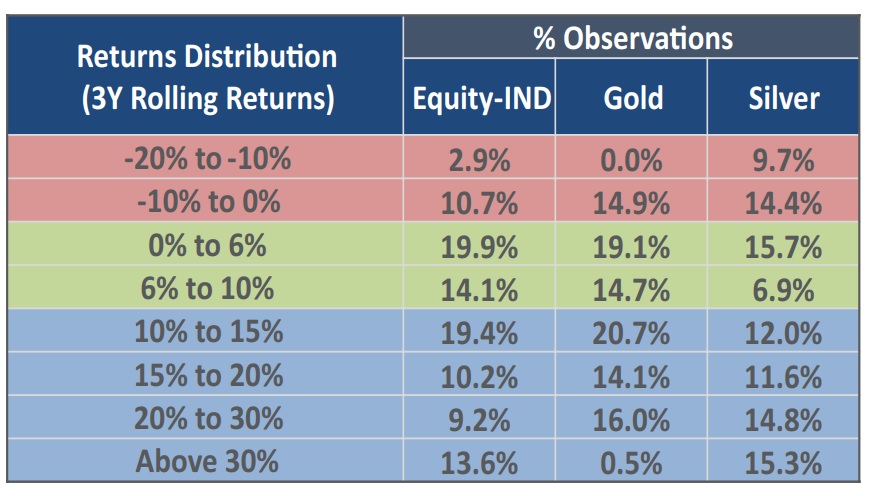

Positive Observations (%) - 3Y | 86.4% | 85.1% | 76.4% |

Note: STD is based on monthly returns, *CAGR is for period 1990 to 31 Oct’ 24; st . Equity-IND is represented by Sensex from 1990 to 2002 and Nifty 50 from 2002 onwards; MCX Spot Gold price in INR from 2006 till date; S&P 500 in INR 1990 onwards; Silver – USD Silver converted in INR. Disclaimer: Past Performance is no guarantee of future Results

The recent fluctuations in gold and silver prices can be attributed to several global events, particularly the US Presidential Election. Interestingly, gold tends to do slightly better before a Republican president is elected and remains flat post-election. Conversely, it underperforms before a Democratic president's election and tracks slightly below its long-term average thereafter. Despite these trends, the variability in outcomes suggests that gold's performance is more closely tied to the policies of the elected administration rather than the party affiliation itself.

Gold and silver posted impressive gains this year amid rising geopolitical conflicts and uncertainty around US Presidential election till Oct’24. But some of that momentum has been lost in early November. Trump's economic proposals on tax cuts and tariff hikes led to expectations of aggressive fiscal policies, which in turn resulted into hardening of US treasury yields, rise in dollar index and hence dampening the investor enthusiasm for gold and silver. Federal Reserve's mixed signals on future interest rate cuts and China’s policy announcements falling short of expectations have further put some pressure on bullions.

Looking ahead, the gold and silver are poised to navigate through diverse influences. Factors such as the US administration's economic policies, the Fed's stance on monetary policy, and broader geopolitical risks will be key in shaping the future direction of gold and silver prices.